The insurance sector is under pressure as consumers shift their spending to tap into new technological frontiers. At the same time, InsurTech startups are making it easier than ever for customers to find and purchase insurance products online.

To succeed in this environment, insurers need to anticipate and embrace change.

We see an expedited adoption of remote signing and customer servicing technologies, tools for digital collaboration, and new innovative digital products.

As digital becomes the new normal, what lies ahead, and what should insurance leaders prepare for? Here are 16 digital transformation trends that will shape the insurance sector in the next few years:

Enterprise IT is evolving

Enterprise IT is evolving from a cost center to a strategic enabler

In the past, insurance companies would IT as a way to cut costs. Now, it's all about how technology can help organizations drive growth and improve customer engagement.

1. The rise of low-code/no-code development in enterprise IT

One of the most pronounced trends within the normalization of low-code/no-code development in enterprise IT. While in the SMB segment, no-code tools became the new norm, enterprises, for the most part, continued to rely on the traditional development projects powered by internal resources or external integrators.

However, this is now changing as vendors start to offer mature, enterprise-grade no-code tools focusing on security and compliance. So enterprises can now ooffload some of the development burden to line-of-business users while maintaining governance and control.

Such tools owe their growing popularity to the fact that they solve some burning issues facing IT teams. No-code tools amplify overstretched internal resources, reduce backlogs, and improve productivity.

The most crucial quality that makes no-code tools extremely attractive is accelerated time to market for new digital applications and products compared with traditional development projects. With no-code tools, Insurers can now deliver better apps at a quicker rate, improve customer experience, and enhance overall service quality.

2. The continued rise of the API economy

An Application Programming Interface (API) is a set of rules that govern how one piece of software interacts with another. In recent years, there has been a proliferation of APIs as companies seek to open up their data and functionality to third-party developers.

In the insurance industry, APIs are being used to enable the development of new digital products and services. For example, some insurers are using APIs to provide real-time quotes to customers, while others are using them to power chatbots and other digital customer service tools.

APIs (Application Programming Interfaces) will continue to grow in popularity and usage as the need for digital integration increases. Many traditional businesses are now looking to open up their data and systems to third-party developers in order to create new digital experiences and business models.

This trend is being driven by the need for agility and faster time-to-market as well as the desire to tap into new revenue streams. In the insurance industry, we are seeing a growing number of insurers launching APIs to allow third-party developers to build new apps and services on top of their core systems.

Going forward, we expect to see more insurers making use of APIs as they look to capitalize on the growing demand for insurance products that are delivered through digital channels.

3. The rise of "headless tech"

It might sound somewhat gruesome, but "headless tech" is quite harmless and has been with us for a while.

The most well-known example of headless technology can be found in website development. Traditional websites have a back-end and a front-end as well as a graphical user interface.

In a way, headless tech is a complementary trend that goes hand in hand with no-code tools for developing customer-facing front-ends. Insurers can now separate their front-end presentation layer from their back-end data functionality to create custom digital experiences.

In Insurance, this is particularly important, as back-ends are mired with legacy technology problems that are, for the most part, make them incompatible with the modern front-end experiences customers expect.

By separating customer-facing front-ends and back-end processes while ensuring that the data flows freely between the two is another trend that we will see getting stronger in the near future. Our prediction is that we will see more insurance products and applications that adopt the same principle.

4. Hybrid cloud architecture is on the rise

According to Mordor Intelligence, the hybrid cloud market is expected to reach USD 128.01 billion by 2025, at a CAGR of 18.73% over the forecast period 2020 - 2025.

Organizations increasingly adopt the hybrid cloud as they aim to leverage the advantages of both cloud and public clouds.

Hybrid cloud architectures improve both speed and flexibility by allowing organizations to go back and forth between their own tools and the cloud providers' toolkits.

5. The continued rise of customer data

As digital channels continue to proliferate, the volume of customer data that is being generated is increasing at an exponential rate. This presents both a challenge and an opportunity for insurers.

On the one hand, insurers need to find ways to effectively manage and store this ever-growing volume of data. On the other hand, insurers that are able to effectively leverage this data will be able to gain a competitive advantage.

In the coming years, we expect to see more insurers making use of advanced data analytics tools to extract insights from customer data. These insights can then be used to improve customer experience, underwriting, and claims handling.

The technology trends such as the rise of no-code tools and "headless tech" mean that financial service organizations can keep their legacy architectures intact while improving the digital experience for customers and employees at the same time.

Customer experience takes center stage

The insurance industry has always been a customer-centric business, but the rise of digital technology has given customers more power than ever before.

Customers are now able to shop around for the best prices, compare different products, and find the most suitable insurer for their needs with just a few clicks.

In response to this, insurers are increasingly focused on providing a superior customer experience. This includes offering more personalized products and services, as well as making it easier for customers to do business with them through digital channels.

6. Delivering tailored digital products

Tailoring a product to an individual's need is not a new concept, but it is one that has been made possible by advances in technology, particularly data analytics and machine learning.

In the past, insurers would have needed to rely on customer surveys and other forms of market research to gather the necessary data points. But now, with the proliferation of data, insurers can draw on a much wider range of sources, including social media, web browsing data, and even wearable devices.

This wealth of data gives insurers the ability to develop a much deeper understanding of their customers and deliver products that are far more closely aligned with their needs.

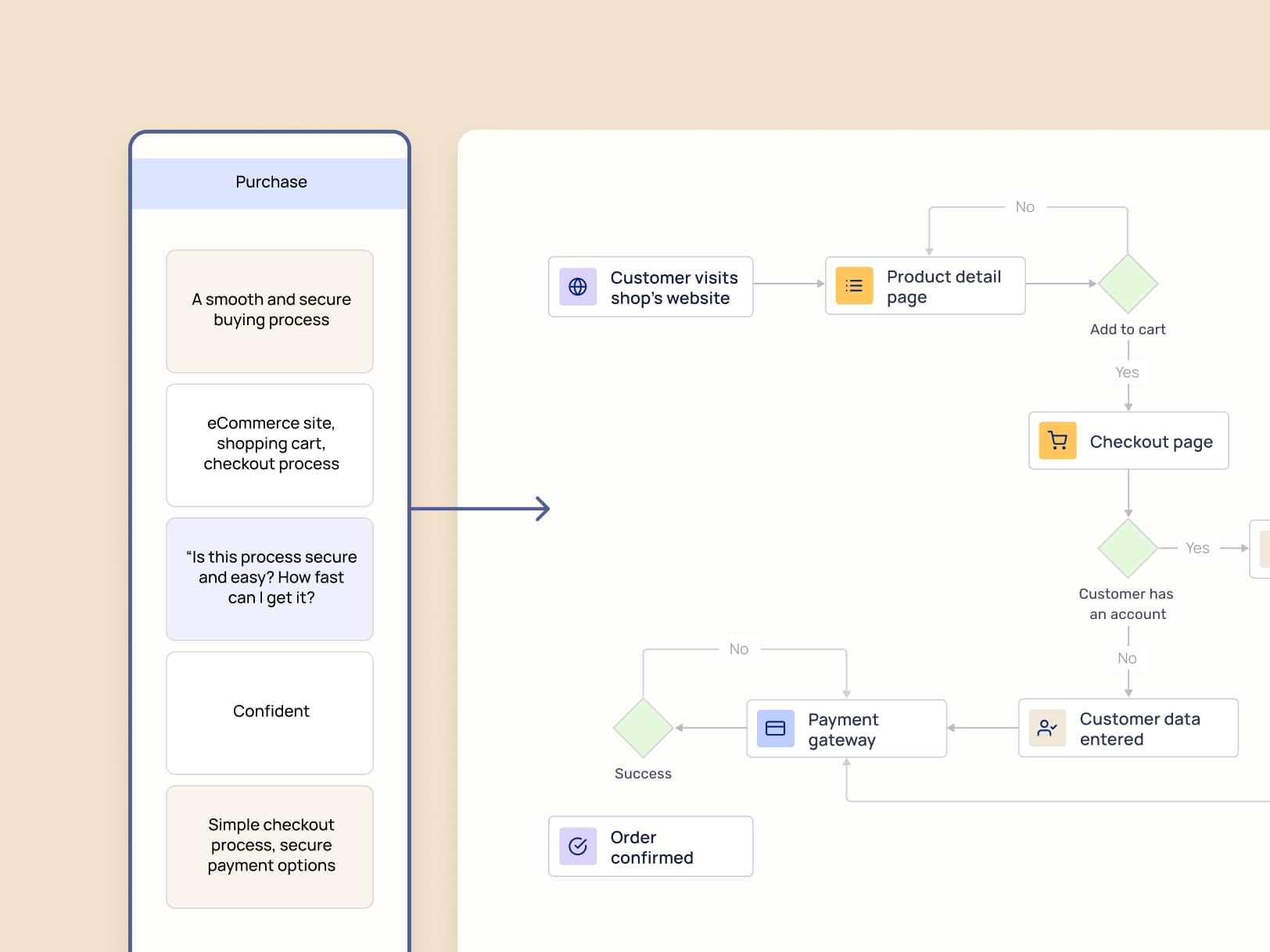

7. The rise of customer self-service

One of the biggest trends in insurance is the growing expectation among customers for self-service. Thanks to the proliferation of digital channels such as online portals and mobile apps, customers now expect to be able to do more for themselves without having to pick up the phone and speak to a customer service representative.

In response to this trend, insurers are increasingly investing in digital self-service tools such as online quote generators and chatbots. These tools allow customers to get the information they need without having to wait on hold or navigate through complex processes.

What's more, by handling simple tasks themselves, customers are freeing up time for insurers to focus on more complex issues.

Now, agents and brokers are increasingly moving to digital tools, while the self-service digital channel is also rising due to skyrocketing customer demand. A late-April 2020 survey of European insurance executives found that some 89 percent of respondents expect a significant acceleration in digitization, and most also anticipate a further shift in channel mix.

[.figure]89%[.figure]

[.emph]expect a significant acceleration in digitization[.emph]

8. The expansion of digital channels

Insurance traditionally has been sold through physical channels, including agents or brokers, resellers, offices, and call centers. But now, the digital channel is gaining the edge. As customers become more comfortable conducting business online, insurers are expanding their digital customer channels to meet this demand. In addition to traditional web and mobile self-service channels, insurers are now offering chatbots, virtual customer assistants, and even voice-based customer service.

Now, agents and brokers are increasingly moving to digital tools, while the self-service digital channel is also rising due to skyrocketing customer demand. A late-April 2020 survey of European insurance executives found that some 89 percent of respondents expect a significant acceleration in digitization, and most also anticipate a further shift in channel mix.

Increasingly, offline processes are transitioning into the digital realm. Even products that sometimes require offline execution, such as physical signatures and medical underwriting, are increasingly transitioning to digital with the help of technology such as legally binding eSignatures or face-recognition and telemedicine.

The rise of new business models

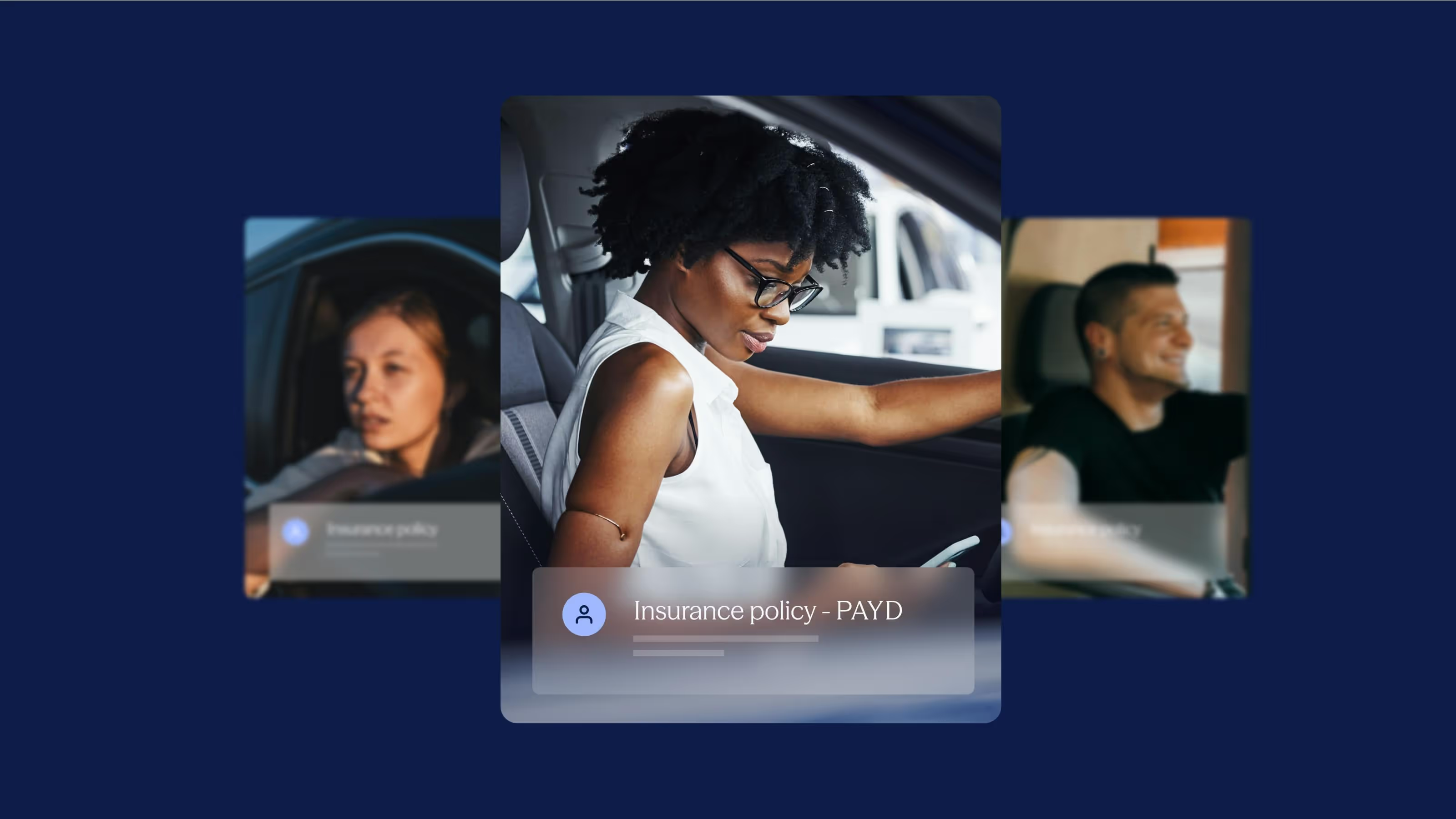

9. The growth of usage-based insurance

Usage-based insurance (UBI) is a type of insurance that charges customers based on their actual usage, rather than an estimate of their usage. The most common form of UBI is pay-as-you-drive insurance, which charges customers based on the number of miles they drive.

UBI is becoming increasingly popular as a way to offer more affordable insurance to low-mileage drivers. In addition, UBI can also be used to encourage customers to change their driving habits in order to reduce their risk of accidents.

For example, some insurers offer discounts to customers who use telematics devices to track their driving habits and prove that they are safe drivers.

10. The growth of insurance telematics

Telematics is a technology that enables the tracking of data about a vehicle's movements, and it is increasingly being used by insurers to gather data about their customers' driving habits.

The adoption of telematics-based insurance products is being driven by the desire to offer more personalized pricing to customers. By knowing exactly how and when a customer drives, insurers can better assess the risk involved and price their products accordingly.

In addition, telematics can also be used to detect fraudulent behavior. For example, if an insured driver is found to be deliberately driving in a way that is likely to cause an accident, their insurance policy could be voided.

The evolution of culture and technology in the workplace

11. Work from home is here to stay

Work from home has been an exception, rather than the rule, for a very long time. However, it seems that even after the COVID-19 pandemic is behind us, the work from home culture will stay with us.

According to a recent survey by Bloomberquint, the number of workers who say they won't go back to the office full time has increased significantly, with over a quarter of those surveyed planning to continue working remotely at least half the time after the pandemic is over.

For insurers, this means that they need to support their employees to complete their tasks remotely. Manual workflows have been outdated even before the pandemic, but (with some minor exceptions) in the post-pandemic world, there is no place for paper-based workflows that require employees' physical presence.

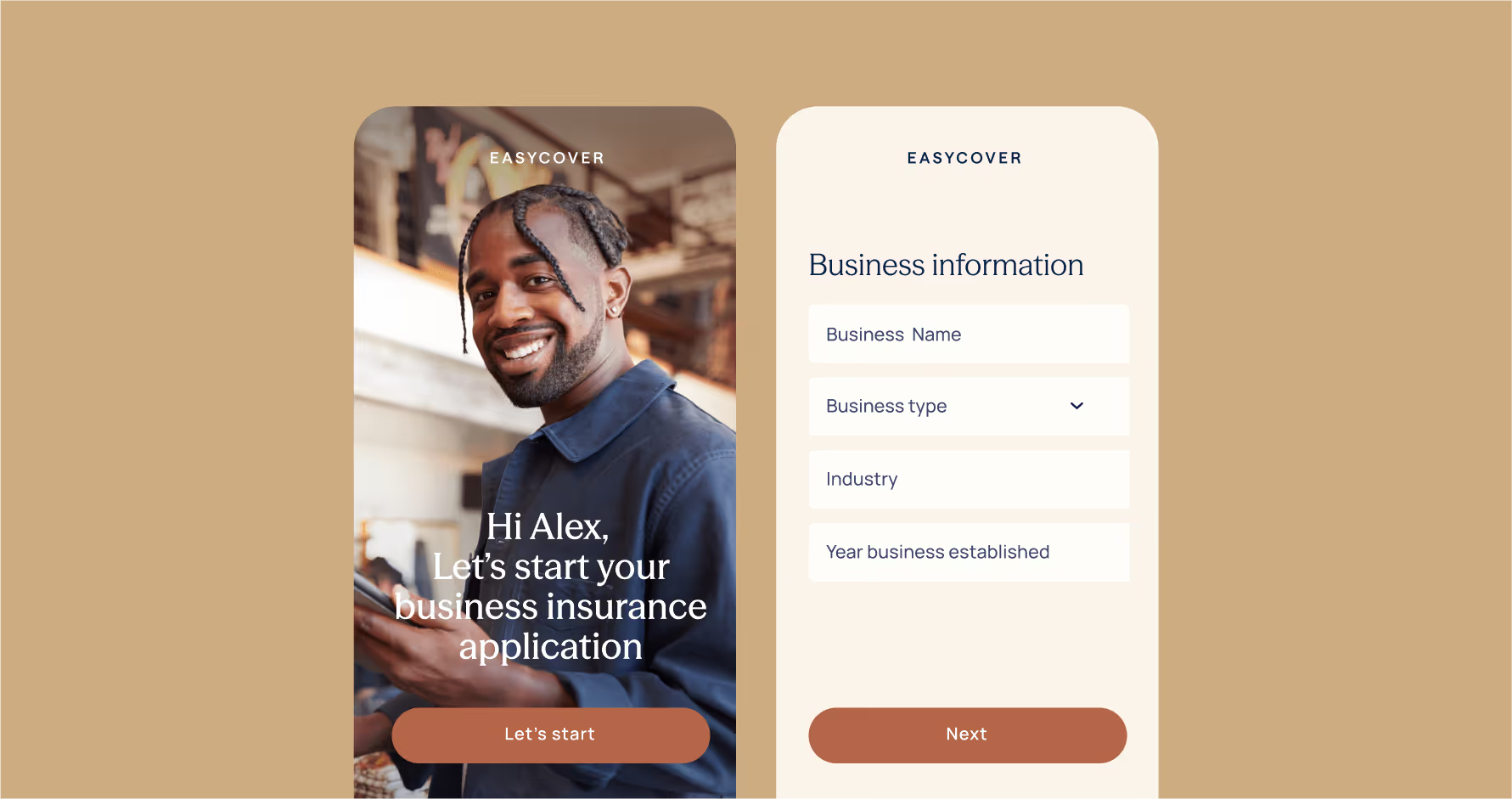

12. The rise of digital data collection

Inefficient paper-pushing has been the norm in the insurance industry for centuries. However, this is no longer feasible. Insurers cannot continue to treat inefficient paperwork as a necessary evil and need to find solutions to improve customer experience on that front.

Recent study by Bain & Company found that, on average, insurance companies only collect about 60 percent of the data they need to underwrite a policy. The other 40 percent is either never collected or collected too late in the process.

This not only leads to customer frustration but also exposes insurers to greater regulatory risk. In an increasingly digitized world, insurers need to be able to rapidly collect, analyze and act on data.

And that is where digital customer data intake comes in.

As eSignatures and digital forms are being normalized, customers expect to complete nearly all (if not all) actions with their insurer remotely via digital tools - from account opening to policy renewals.

By transforming the way they collect data and signatures from customers, insurers can make the process more efficient, improve customer satisfaction and reduce regulatory risk.

New ways to manage risk

IoT technology keeps gaining momentum in the insurance industry, including risk assessment and underwriting. Most crucial of all, IoT theoretically can empower insurers to move from their traditional role in risk protection to risk prevention.

13. The rise of predictive analytics

Predictive analytics is a type of artificial intelligence that is used to make predictions about future events. This technology is increasingly being used by insurers to identify risk factors and price their products accordingly.

For example, if an insurer knows that a customer is more likely to have an accident at certain times of the day or in certain weather conditions, they can price their product accordingly. . Introduction

14. IoT increases the need for streaming analytics to innovate

Internet of Things supports insurance technology by providing accurate and real-time data. This improves the accuracy of risk assessment and gives insurance holders the ability to gauge their policy pricing accurately.

However, IoT implementation for risk assessment has many challenges. One of which is analytics. Data provided by IoT is real-time; unfortunately, real-time analytics leave much to be desired. We expect a lot of innovation in this space as the market demand for IoT has driven analytics grows.

15. Increased focus on algorithmic risk assessment

Artificial Intelligence plays a significant role in the insurance industry. The AI-based tools provide solutions for insurance operations and claims settlement teams.

But Machine Learning has value beyond claims processing; it has the power to help insurers automate the entire process. As files are becoming increasingly digitized, they can be easily analyzed using AI algorithms, eliminating manual processing entirely.

This improves processing speed and accuracy, not only in policy administration but also in risk assessment. Machine learning and AI technologies are going to continue growing in popularity as risk assessment tools.

16. The shift in culture from legacy to innovation

Insurance has traditionally been a very conservative industry. But it is now rapidly changing with the influx of new blood in the form of digital-first insurers, tech giants, and innovative startups.

There is a pronounced shift in the mindset among insurance leaders and experts, as the need to innovate is becoming apparent to everyone involved. The industry has shifted from a conservative into an increasingly innovation-focused, digital culture.

It is clear that we are headed towards more innovation, better customer and employee experience, increased agility, and innovative applications of existing technologies to age-old insurance problems such as risk-assessment claims processing and policy sales.

The challenges facing the insurance industry

13. Insurers must evolve to compete

Competition is becoming tougher. There are new entrants to the market, such as digital-first insurers and tech giants. At the same time, customers are becoming more demanding, expecting insurers to provide a better customer experience.

In order to compete, insurers need to evolve. They need to become more customer-centric and focus on providing a great customer experience. They also need to adopt new technologies that will help them become more agile and efficient.

The need for speed

In this rapidly changing world, the insurance industry is under pressure to keep up with the pace of change. New entrants to the market are offering new products and services at a much faster rate than incumbent insurers. This means that incumbents need to move faster in order to stay relevant. They need to be able to quickly develop and launch new products, enter new markets, and scale quickly.

In order to be able to do this, insurers need to become more agile. They need to adopt new technologies and processes that will allow them to move faster.

[.emph]Digital transformation is no longer an option for insurers; it is a necessity. In order to compete in this new world, insurers need to embrace digital and use it to their advantage.[.emph]

FAQ

Forget forms. Create digital customer journeys.