.avif)

The global travel insurance market size reached US$ 17.9 Billion in 2023 and is expected to grow to US$ 47.1 Billion by 2032, exhibiting a growth rate (CAGR) of 11% during 2024-2032. This significant growth underscores the expanding need for travel insurance services and the potential benefits of optimizing data intake and FNOL processes to cater to this growing demand effectively.

Despite the critical importance of digital transformation, a 2023 AWS survey found that while 95% of travel executives responded that digital transformation is "very important" or "somewhat important" to their business’s overall strategy and success, their top priority remains the maintenance and upkeep of legacy systems. This highlights a crucial gap between recognizing the need for digital transformation and the actual prioritization and implementation of such strategies within the sector.

In the realm of travel insurance, streamlining the data intake process and enhancing the First Notice of Loss (FNOL) procedure are critical for operational efficiency and improving customer experience. This ebook outlines a general approach to transforming these processes, focusing on strategic improvements and showcasing how technology and strategic planning can transform and streamline the travel insurance claims process.

Industry Challenges in Data Intake and FNOL Processes

The current travel insurance sector faces several challenges that hinder seamless data intake and FNOL procedures. These include:

Siloed and fragmented data intake processes

Insurers often have multiple data intake processes, leading to fragmented claims information housed in different systems. This results in data discrepancies, delays in claims processing, and lack of real-time visibility into the status of a claim.

Moreover, the complexity of managing multiple types of claims across various coverage options leads to inefficiency and customer dissatisfaction. Often, claims handling involves multiple, uncoordinated steps, especially when different product coverages require separate submissions. This can lead to a poor customer experience and inefficiencies for adjusters.

- Inconsistent data formats: Data submitted by customers is often incomplete or inconsistent, making it challenging for insurers to obtain a clear understanding of the claim.

- Manual data entry: Manually entering customer information can lead to human error and increased processing time.

- Lack of real-time data sharing: Insurers often struggle with obtaining timely updates on claims. Lack of real-time communication and collaboration between internal teams, external partners, and customers can lead to delays in claims processing. For instance, if an adjuster needs additional information from the customer or medical reports from a healthcare provider, this process is often slow and cumbersome.

- Lack of integration: Often, the systems used for data intake and FNOL are not integrated, resulting in siloed data and communication breakdowns.

- Limited automation: With minimal automation, insurers struggle to efficiently process large volumes of claims and respond to customers in a timely manner.

- Data silos: The lack of integration between different data systems can hinder the efficient processing of claims and the delivery of personalized customer experiences.

Technological Lag

The slow pace of digital transformation in some segments of the industry results in outdated processes that fail to meet the expectations of today’s digital-savvy customers.

Many insurers struggle with digitalizing the FNOL process. Low adoption rates of digital solutions can result from outdated interfaces, lack of mobile responsiveness, and cumbersome digital workflows.This can lead to a frustrating experience for customers and potential delays in claims processing.

Furthermore, outdated systems can also create security concerns, leaving customer data vulnerable to cyber attacks.

Additionally, the lack of advanced analytics tools and AI capabilities makes it challenging for insurers to make informed decisions and identify patterns that could improve their FNOL processes. The absence of real-time tracking and monitoring tools further hinders the ability to detect potential fraud and mitigate risks.

- Missed opportunities: Due to lack of internal resources, efficiently using publicly available data (e.g., flight data for travel insurance claims) can be a hurdle, limiting opportunities for auto-adjudication of simple claims.

Friction in the Digital Journey

Interruptions in the digital journey, such as requests for additional documentation, can create friction and deter customers from completing the process online.

To address this issue, insurers can leverage digital tools such as e-signatures, online document upload, and automated data extraction. These solutions help streamline the documentation process and reduce the need for manual intervention, resulting in a smoother digital journey for customers.

- Disconnect between multiple touchpoints: customers expect a seamless and connected experience across all touchpoints. However, many insurers still struggle with disconnected systems and processes, leading to a disjointed customer journey.

- Point solutions and integration challenges: Travel insurance companies are increasingly turning to point solutions that specialize in particular aspects of the customer's journey. These can include mobile apps offering instant policy management and claim filing, GPS-enabled services for rapid assistance during travel, and on-demand travel assistance services that provide real-time advice and support. Interactive chatbots and AI-driven interfaces also streamline the customer service experience, allowing for prompt responses to inquiries and assistance with processing claims or amending policies. While point solutions can offer targeted benefits, they often create silos of information which can be difficult to integrate into an end-to-end continuous journey.

Reliance on Call Centers and Third Party Administrators

Excessive dependence on external partners can disrupt the digital journey and increase operational costs.

- Cost Implications of Call Centers: The average cost per customer service call across industries ranges between $2.70 and $5.60. This cost factor is critical for insurance companies to consider as it directly impacts operational budgets. Excessive reliance on call centers for customer service and claims processing can significantly elevate operational costs, making the case for digital transformation and automation even stronger.

- Operational Efficiency: Most call centers aim to answer 80% of calls in under 20 seconds, with efforts to improve this to 90% of calls in under 15 seconds. While these metrics demonstrate a commitment to efficiency, they also highlight the limitations and challenges of managing customer interactions solely through call centers. Streamlining data intake and FNOL processes through digital channels can complement call center operations, reducing wait times and improving overall customer satisfaction.

- Customer Experience and Spending: Customers are likely to spend 140% more following a positive experience compared to a negative one. This statistic underscores the importance of efficient and positive customer interactions, whether through call centers or digital channels. By reducing reliance on external partners and enhancing digital journeys, insurers can significantly improve customer experiences, potentially increasing customer loyalty and spending.

Key Strategies for Data Intake and FNOL Enhancement

To overcome these challenges, leading travel insurance companies are adopting several strategies to enhance their data intake and FNOL processes. First and foremost, insurers are leveraging advanced technologies to integrate data from various sources, automate processes, and reduce manual intervention. These include:

Unified Claims Workflow

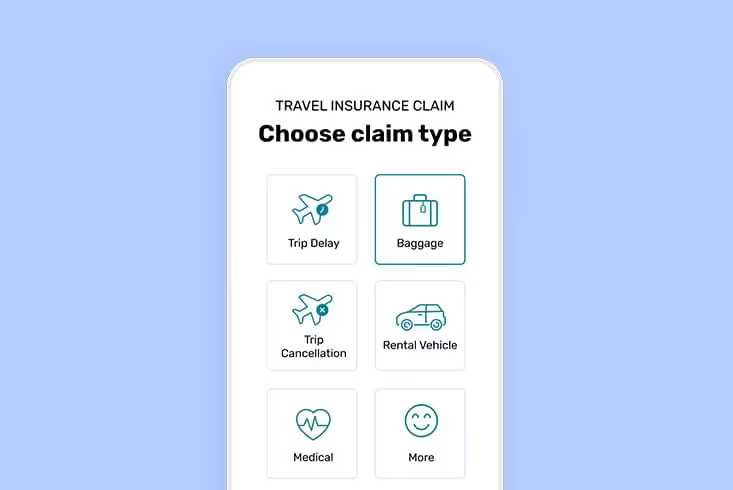

Leading insurers are adopting integrated platforms that consolidate claims processing into a single, streamlined workflow. This approach reduces manual tasks, improves accuracy, and speeds up claim resolution times.

Implementing a unified workflow that seamlessly integrates diverse claim submissions can significantly improve the customer and adjuster experience. Simplifying the claims process makes it easier for customers to file claims and for adjusters to process them.

A key element includes tools that help insurers to unify disjointed data collection processes into a unified, end-to-end workflow, that covers:

- Multi-channel data intake: Customers can submit claims through various channels, including web portals, mobile apps, email, and call centers. Insurers need a unified solution that enables seamless data intake regardless of the channel used by the customer.

- Unified data validation: Data validation is a critical component of the claims handling process. Leading insurers are using advanced tools that automate data validation and verification and prevent common errors in customer-submitted data.

- Automated document management: Insurers often require customers to submit documents, such as medical bills or police reports, as evidence for their claims. Advanced document management tools allow insurers to scan and store documents electronically, minimizing manual handling and improving efficiency.

- Integrated communication tools: Providing timely updates to customers is key for a satisfactory claims experience. Unified workflow platforms offer integrated communication tools that enable real-time communication with customers, keeping them informed about the status of their claim.

- Intelligent Document Recognition (IDR): Using IDR technology, insurers can extract data from various documents and forms to speed up the claims process.

Digital Adoption and Customer Engagement

To address the challenge of low digital adoption, insurers are revamping their online portals and mobile apps to offer intuitive, user-friendly interfaces. Features such as chatbots, AI-driven FAQs, and personalized dashboards engage customers and encourage digital interaction.

Focusing on front-end improvements, such as user experience (UX) enhancements, mobile responsiveness, and dynamic workflows, can increase the adoption of digital FNOL. Providing a seamless and intuitive digital interface encourages customers to utilize online channels.

- Mobile-First Approach: With the increasing use of mobile devices, insurers are investing in mobile applications for customers to submit claims and upload necessary documents on the go.

- Self-Service Customer Portals: Providing customers with self-service portals allows them to track their claims, view policy information, and submit necessary documents without the need for assistance from call centers or third parties.

Empowering customers to self-serve through digital platforms can also improve the claims experience and reduce reliance on external partners. This can include features such as online claim submission, status tracking, and virtual customer support.

- Convenience for customers: By providing self-service options, customers have more control over their claims process and can easily access information at any time.

- Reducing costs: Self-service options also reduce the need for manual processing and decrease reliance on external partners, ultimately reducing costs for insurers.

Reducing Friction in the Digital Journey

Incorporating features like "save and continue," mobile-friendly document uploads, and streamlined workflows can ensure a smoother process for customers. Minimizing disruptions in the digital journey is crucial for maintaining customer engagement.

Some areas of focus for reducing friction in the digital journey include:

- Digital Data Intake: Insurers can improve online form design by implementing auto-fill, eSignature, document upload, and error-free validation features to make it easier for customers to submit accurate information no matter which channel they chose.

- Omnichannel Integration: Integrating different channels, such as chatbots or email notifications, within the digital journey ensures a seamless experience across various touchpoints for customers.

- Real-Time Communication: Utilizing real-time communication tools, such as instant messaging or video chat, allows for quicker and more convenient support for customers during the digital claims process.

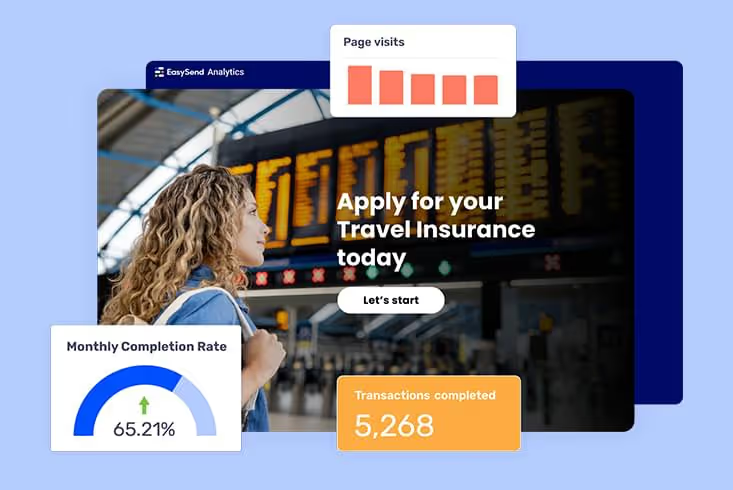

Overall, by prioritizing front-end improvements and reducing friction in the digital journey, insurers can successfully engage customers and encourage them to utilize online channels. This not only improves customer satisfaction but also results in cost savings for insurers by reducing the need for manual processes. With self-service portals and a seamless digital journey, customers can easily submit claims and upload necessary documents on the go, making the process more convenient and efficient for both parties involved.

Leveraging Data Analytics

Advanced data analytics and machine learning algorithms are being utilized to analyze claims data, predict trends, and identify fraud more effectively. This not only improves operational efficiency but also enhances risk assessment and management.

Utilizing real-time analytics and reporting tools can help insurers gain insights into their data, identify patterns, and make informed decisions to improve their processes continuously.

- Advanced reporting and analytics: To continuously improve their claims handling processes, insurers need to track and analyze data on claim performance. Unified workflow platforms provide advanced reporting and analytics capabilities that allow insurers to identify areas for improvement and make data-driven decisions.

Automation of Simple Claims

Some insurers have successfully automated the adjudication of straightforward claims, such as minor travel delays or cancellations, leveraging real-time data and predefined criteria for instant resolution.

Automating the adjudication of simple claims by using publicly available data, such as flight information for travel insurance, can enhance operational efficiency. This approach allows for quicker claim resolution and improved customer satisfaction.

This allows for a more efficient and seamless experience for customers, while freeing up resources to focus on handling more complex claims.

- Leveraging real-time data: By utilizing real-time data such as flight information or weather reports, insurers can automatically process simple claims without the need for manual intervention. Insurers can also leverage third-party data sources, such as electronic medical records or government databases. This helps save time and resources while minimizing the risk of human error.

- Utilizing open-source data: Open-source data, such as social media posts and public records, can also be utilized to cross-reference information provided by claimants and detect any discrepancies. This further aids in identifying potentially fraudulent claims.

- Implementing predefined criteria: Insurers can also establish clear and defined criteria for automated claims, ensuring consistency and accuracy in decision-making.

Minimizing Reliance on External Partners

Developing in-house capabilities to handle claims digitally reduces the need for call centers and third-party administrators (TPAs). This shift can lead to cost savings and a more controlled and consistent customer experience.

- Investing in technology: Insurers can invest in robust and modern technology, such as artificial intelligence and machine learning, to handle claims processing internally. This allows for faster decision-making and reduces the risk of human error.

- Streamlining processes: By streamlining internal processes and reducing reliance on external partners, insurers can also improve turnaround times for claims handling and reduce costs associated with outsourcing.

Cross-Functional Data Integration

By integrating data from various sources, including multi-channel customer communications, publicly available data such as flight data and weather information, as well as data from internal systems of record, insurers can offer dynamic coverage options and proactively address potential claims scenarios. This not only improves the customer experience, but also reduces the likelihood of fraudulent claims.

- Proactive and personalized coverage: With cross-functional data integration, insurers can offer personalized coverage options based on real-time data and individual risk profiles. This allows for a more tailored and relevant insurance experience for customers.

- Fraud detection and prevention: By analyzing integrated data, insurers can identify patterns and anomalies that may indicate fraudulent activity. This enables them to take proactive measures to prevent fraud and protect their bottom line.

Enhanced Customer Communication Channels

Implementing omnichannel communication strategies has enabled insurers to offer consistent and efficient customer service across email, SMS, social media, and chat platforms.

This not only improves the overall customer experience, but also facilitates faster claims processing.

- Instant communication: By utilizing multiple communication channels, insurers can instantly notify customers about their claim status and any relevant updates. This reduces the need for manual follow-up and streamlines the claims process.

- Improved transparency: With omnichannel communication, customers have access to real-time updates and can track the progress of their claims. This enhances transparency and builds trust between insurers and their customers.

- Efficient data collection: By leveraging different communication channels, insurers can gather information from various sources to validate claims and make informed decisions. This speeds up the claims process and minimizes errors.

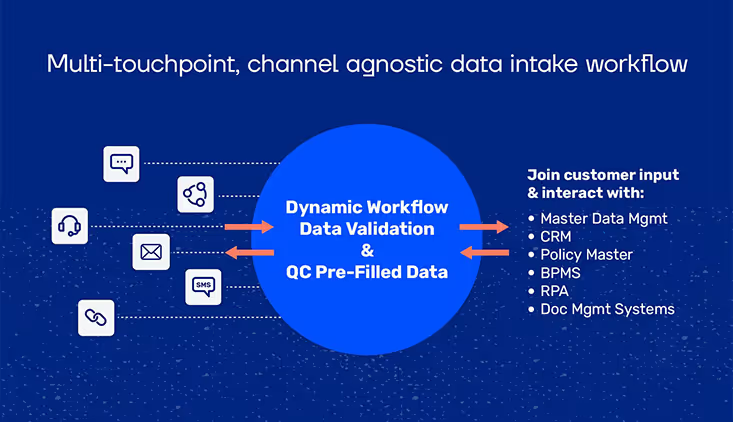

Introducing Dynamic Data Intake Workflows

Digital transformation is set to remove friction and alter the entire insurance process, improving the customer experience all the way from purchasing a policy through to processing claims, issuing payouts, and making reimbursements.

Transforming the travel insurance data intake and FNOL process requires a multifaceted strategy that addresses digital adoption, process streamlining, and efficient data use. The transformation of disjointed customer data intake into streamlined, dynamic workflows is not just a vision but a tangible reality that can be achieved with the right approach and technology.

EasySend exemplifies how this transformation can be realized, offering a robust platform that turns complex and siloed data collection processes into cohesive, efficient workflows. By bridging the gaps between manual and digital processes, and unifying fragmented digital initiatives, EasySend empowers businesses to enhance digital adoption, improve customer experiences, and optimize operational efficiency.

By solving the challenges of disjointed customer communications and piecemeal data collection, EasySend enables businesses to harness the full potential of their data, streamline complex processes, and deliver seamless customer journeys from the first touchpoint to the last.

Through dynamic customer data intake workflows, travel insurers can turn their data management challenges into a competitive advantage, ensuring that they are well-positioned for growth and success in the digital era.

.avif)

.avif)

.avif)