Neobanks are disrupters in the fintech world, offering a wide variety of apps and websites that simplify, streamline, and personalize online banking. Although they don’t offer the same scope of financial services as a traditional bank, they often cater to a specific niche and promise easier, affordable, and more transparent service.

Neobanks are popping up like mushrooms after the rain all over the globe, especially after the pandemic as the public was forced to conduct more business online. According to a recent report by Exton consulting, there were 60 neobanks worldwide in 2018. By 2020, there were 256, with many more ready to be launched. But why are neobanks popular? Do they really pose a threat to traditional banks? What can traditional banks do to compete with these new and innovative players in the financial market?

Neobank vs digital bank vs traditional bank

Before we look at the comparative advantages and disadvantages of neobanks, let's first define what neobanks are and how they are different from traditional and digital banks. First and foremost, neobanks don’t have physical branches at all—they’re entirely mobile-focused. That makes them different than digital banks which are simply the digital arm of banks that also have a network of physical locations.

Traditional banks are also weighed down by legacy systems that make it difficult for them to meet the expectations of the modern consumer, especially in the younger, digitally-native market. Neobanks don’t have those limitations and stand out with their simple, intuitive interfaces, and perks like low-cost credit or cash-back rewards.

Not all of the cards are lined up in favor of neobanks—traditional banks have a higher level of public trust, more funding, and a wider range of products and services. However, that doesn’t mean that they don’t need to pay attention—neobanks have significant advantages that they can’t afford to ignore.

Advantages of neobanks

Neobanks have a lot going for them including the following key advantages:

Lower costs

Without physical locations and the human resources needed to staff them, the overhead at neobanks is significantly lower than at traditional banks. Neobanks pass the savings on to their customers, offering lower rates and minimal markups that make them much more affordable than traditional banks, which is a critical consideration in lower-income communities and countries.

Customer experience

Traditional banks aren’t known for offering a stellar customer experience. Limited by inflexible legacy systems, they often use clunky, repetitive forms, complex and tedious processes, and have poor customer service.

Neobanks, on the other hand, emerged from the tech sector bringing tech agility and customer focus with them. They are not bound by legacy systems or a rigid organizational culture. Therefore they can offer user-friendly interfaces, easily make changes, and develop new tools to meet customer needs and address new market opportunities.

Innovative technology

Neobanks were born in the fintech world and advanced tech like AI and machine learning are part of their DNA. They go above and beyond mobile banking basics, offering helpful chatbots, personalized recommendations, easy but secure authentications, and more.

Serving the unbanked and “under-banked” market segments

Rather than focusing their marketing efforts on winning over traditional banking customers, many neobanks focused on the “unbanked”, or people who didn’t use banking services, usually because they could not afford the high fees or were off-put by the cumbersome onboarding processes. Neobanks offer the unbanked affordable interest rates and service fees, and also have made the paperwork and onboarding processes less overwhelming. Some neobanks have also strategically targeted other lower value market segments like freelancers and gig workers that have grown significantly in recent years, or even specific immigrant communities, addressing their unique needs and concerns and offering them service in their native language.

Popular neobanks

There are now hundreds of neobanks to choose from, each with its own unique advantages and disadvantages. Below are some of the market leaders in the United States and around the world.

Chime

With >12 million customers, Chime is one of the biggest and most established neobanks in the US market. It offers checking and savings accounts with no monthly fees, and even a secured credit card that customers can use to build credit. There is no minimum balance, maximum amount for earning interest, or monthly costs. Chime spending accounts give customers access to ATMs, and they allow cash deposits at big retailers—something many other neobanks don’t offer. With so many perks, it’s clear why so many customers love Chime.

Varo

Varo Bank started out by partnering with traditional banks and then became an independent, nationally chartered bank in 2020. Varo offers checking, savings, and cash advances to its 4 million customers, as well as perks like free ATM access, no monthly fees, cashback at specific retailers, and no foreign transaction fees.

SoFi (Social Finance)

This neobank started out as a student loan refinance company but recently received a bank charter. Its combination account for spending and savings has no account fees for overdraft, ATM usage, or monthly maintenance. SoFi customers can earn interest, take out loans, trade cryptocurrencies, get a retirement account, and even access both active and automated investing.

Dave

Originally a paycheck advance company, Dave now offers checking accounts in addition to interest-free small advances on paychecks. It has attracted over 10 million customers by offering more than just a friendly name—Dave also helps customers budget and even search for side jobs to supplement their income.

Revolut

Revolut is one of the top contenders outside the US. Based in the UK, Revolut targets international travelers by offering competitive exchange rates and a debit card that works in 100+ currencies. It also makes it easy to transfer funds to other Revolut users all over the world and earn interest on savings, and even offers overseas medical insurance on accounts with a monthly fee.

Nubank

Neobanks meet a key need in emerging markets as can be seen in the performance of the Brazilian behemoth Nubank which boasts 35 million customers in Brazil and many more worldwide. Nubank offers digital accounts, personal loans, life insurance, investments, and a credit card controlled solely through a mobile app that lets users track transactions in real-time, as well as contact customer support and conduct other activities.

Can traditional banks compete with neobanks?

Although they had some competition from one another, traditional banks were essentially a monopoly. Due to the hassle of transferring from one bank to another, customers generally stayed with their bank for life. Traditional banks didn’t have to offer excellent customer service or easy processes to what was essentially a captive audience.

[.emph] With neobanks in the field, that is no longer the case—traditional banks have to invest significantly in their digital transformation and in creating a more customer-centric culture. [.emph]

Some traditional banks are focusing on integration and partnering with front-end-focused neobanks that don’t have an independent banking license to create branded, innovative banking offerings.

Other banks are simply adopting a digital approach and upping the ante in their digital transformation to keep pace with the new players. Things that banks can do to enhance their digital transformation include:

- Offer omnichannel service

Customers expect service providers, including banks, to meet them where they are, whether that’s on their preferred social media platform, a messaging app, or over the phone. Neobanks typically provide this type of omnichannel support, and traditional banks should as well.

- Focus on the user experience

Neobanks offer a user experience that goes above and beyond. Not only are processes and actions simple and intuitive, but they’re also designed to delight users at every step of the way. Traditional banks should follow their lead. Not only will doing so make them more competitive, but it will also help allay the perception of stodginess often associated with traditional banking.

- Use no-code platforms

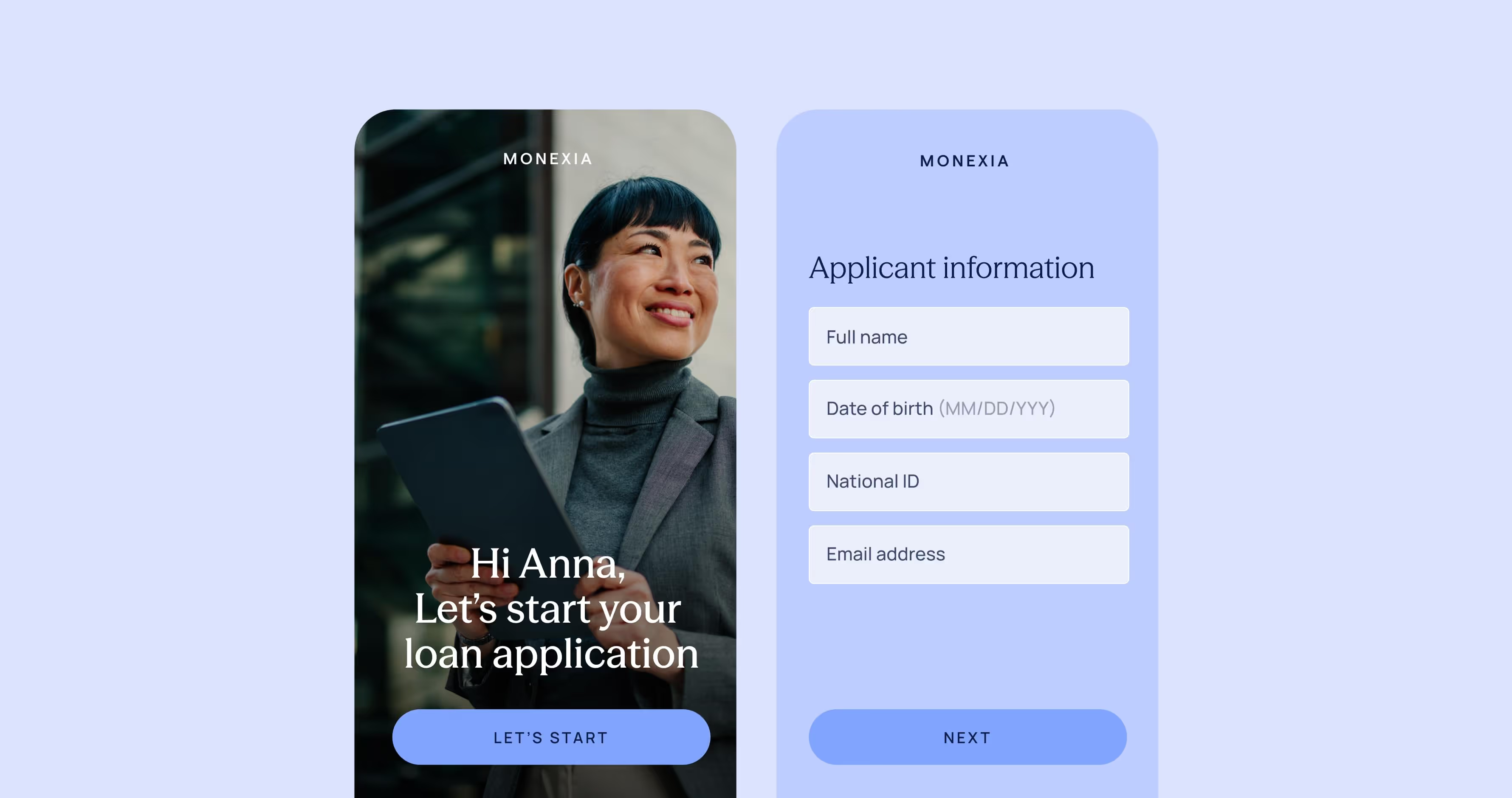

No-code platforms are a key element in this process. No-code and low-code platforms make it easy for traditional banks to create new applications and implement features like e-signatures without going through a labor-intensive development cycle. Instead of waiting for an overloaded IT team to implement every project or change, with a no-code platform, customer-facing staff with minimal technical expertise can address consumer demand quickly and easily, without risk to legacy systems. Using templates and ready-made components, they can deliver new digital products faster in order to meet changing customer needs and stay relevant.

The future of banking and the role of neobanks

The future of banking is digital and mobile, and neobanks are uniquely positioned for growth. Neobanks and challenger banks are pushing older institutions to embrace digital customer experience in order to remain competitive. This is a challenge for traditional banks, but it also opens opportunities to reach new markets and develop new services. And it looks like neobanks are here to stay. In the future, they are likely to advance innovation in banking both as competitors and partners of traditional banks.

FAQ

Forget forms. Create digital customer journeys.