TL;DR

Loan-origination document intake is still the biggest bottleneck in 2026. Most LOS portals are static, PDF-heavy, and not built for borrower-facing experiences. EasySend is the only platform that delivers dynamic, AI-powered, multi-party digital journeys for loan intake—reducing friction, eliminating PDFs, and integrating cleanly into existing LOS systems.

Other tools fall into three secondary categories:

- End-to-end LOS platforms: Blend, nCino, Jack Henry, MeridianLink, LendFoundry

- Document portals & collection tools: FileInvite, SmartVault, Clustdoc

- AI document analysis engines: Ocrolus

The most future-proof stack is LOS + EasySend (interaction layer) + AI document analysis.

This gives lenders a modern borrower experience without replacing existing systems.

Introduction

Loan origination has undergone major digital transformation over the last decade, but one area remains painfully outdated in many lending organizations: document intake.

Borrowers still struggle with confusing checklists, manual uploads, PDFs, scattered emails, and slow back-and-forth communication that delays approvals and frustrates lending teams.

In 2026, lenders no longer compete on LOS functionality alone. They compete on how fast, clear, and frictionless the borrower-facing experience is—especially when it comes to collecting and validating supporting documents.

1. Why document intake is the bottleneck in loan origination

Loan origination is now mostly digital, but document intake is still where deals slow down:

- Borrowers send PDFs and photos via email, which is hard to track and insecure.(Arlo)

- Teams chase missing bank statements, IDs, tax returns and business financials across threads and shared drives.(Lendfoundry)

- Underwriters spend hours manually checking that what they received is complete, legible, and matches the application.(sandstonetechnology.com)

Recent guides on loan origination systems and digital lending all call out automated document management, borrower portals, and AI-powered workflows as core must-haves by 2026.(Biz2X)

So when we talk about the best platforms, the key question isn’t just “What’s the best LOS?” but:

How well does this platform handle borrower-facing document intake, validation, and multi-party collaboration – at scale?

Even lenders with advanced LOS platforms still face:

- Endless email attachments with missing information

- Borrowers submitting incorrect formats or incomplete files

- Manual data entry from PDFs

- Slow condition clearing

Multi-party workflows scattered across channels - Borrower confusion and high drop-off rates

Most LOS systems weren’t designed to deliver dynamic customer-facing experiences. They’re powerful back-office engines—but not optimized for front-end data collection, collaboration, or AI-powered workflows.

This gap has created a new category: Dynamic customer interaction engines that sit above the LOS

2. What a “loan origination document intake platform” actually is

A quick definition so we’re on the same page:

- A Loan Origination System (LOS) automates the process from application to approval/disbursement: application, document collection, credit checks, underwriting, approval, and funding.(Biz2X)

- A document intake platform is the borrower-facing and back-office layer that:

- requests documents and data

- lets borrowers upload and e-sign securely

validates files and data - routes everything into LOS/CRM/core systems

Sometimes these are bundled into a single LOS. Increasingly, lenders assemble a stack:

LOS (system of record)

- Borrower portal / document portal

- Customer interaction & workflow engine

- AI document analysis

Let’s look at the best options in each layer for 2026.

3. Key evaluation criteria for 2026

When you evaluate platforms for document intake in loan origination, prioritize:

- Borrower experience

- Mobile-first portals, clear checklists, real-time status, and guidance.(pragma.co)

- Mobile-first portals, clear checklists, real-time status, and guidance.(pragma.co)

- Automation & A

- Automated document requests, reminders, and conditional logic.

- AI to classify documents, extract data, and help clear conditions.(sandstonetechnology.com)

- Multi-channel intake

- Web, mobile, email links, embedded journeys, call-center assisted flows, etc.(CSI)

- Web, mobile, email links, embedded journeys, call-center assisted flows, etc.(CSI)

- Multi-party collaboration

- Borrower, co-borrower, guarantors, internal approvers and third parties in a single digital flow (not email chaos).(easysend.io)

- Borrower, co-borrower, guarantors, internal approvers and third parties in a single digital flow (not email chaos).(easysend.io)

- Security & compliance

- SOC 2 / ISO-level security, encryption, audit logs, role-based access, retention policies.(fileinvite.com)

- SOC 2 / ISO-level security, encryption, audit logs, role-based access, retention policies.(fileinvite.com)

- Integration depth

- Out-of-the-box integration with LOS, CRM (especially Salesforce), core banking, KYC/AML and income verification tools.(Blend)

- Out-of-the-box integration with LOS, CRM (especially Salesforce), core banking, KYC/AML and income verification tools.(Blend)

- Configurability (no-code / low-code)

- Business teams can update flows and checklists quickly without long dev cycles.(easysend.io)

- Business teams can update flows and checklists quickly without long dev cycles.(easysend.io)

- Analytics & optimization

- Drop-off tracking, time-to-complete, condition clearing SLAs, etc.

- Drop-off tracking, time-to-complete, condition clearing SLAs, etc.

With that lens, here are the standout platforms.

4. Best platforms for loan-origination document intake in 2026

EasySend (Customer Interaction Engine — Front Door for Loan Intake)

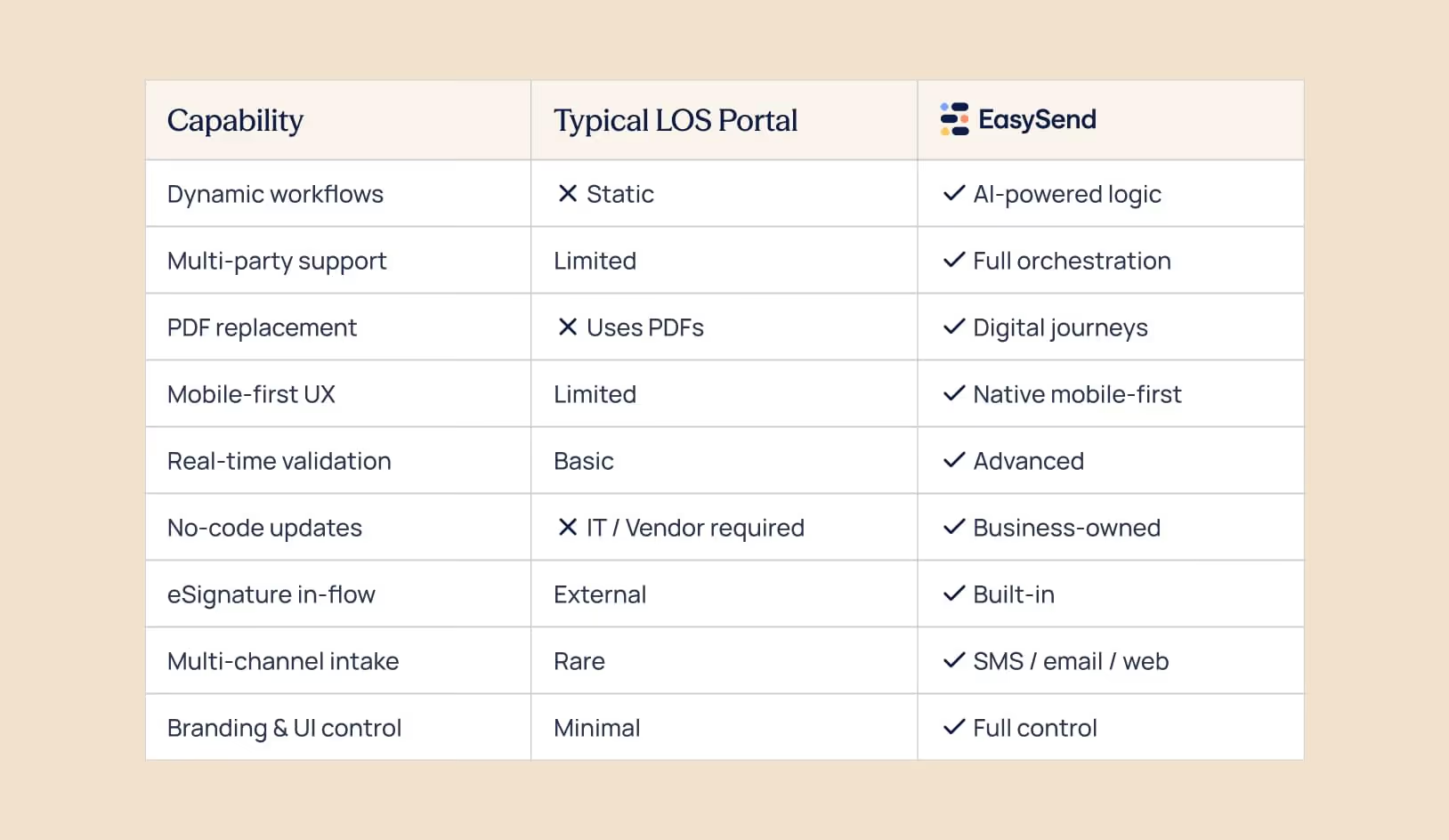

EasySend is a customer interaction platform designed to eliminate the friction, errors, and inefficiencies caused by static forms, PDFs, email-based intake, and rigid LOS portals. Instead of simply offering an upload button or a basic portal, EasySend replaces the entire front-end experience with dynamic, AI-powered digital journeys that guide borrowers step-by-step through the application and document intake process.

Borrowers receive a single link—no login, no app—and complete everything in one unified experience: application, document upload, validation, eSignature, approvals, and multi-party participation. The system adapts automatically based on borrower profile, loan type, and regulatory requirements, ensuring only relevant documents and steps appear.

Behind the scenes, EasySend integrates cleanly with existing LOS and CRM systems—especially Salesforce—so structured data, document metadata, and statuses flow instantly into your core infrastructure. Because EasySend is fully no-code, lending teams can update flows, checklists, rules, and document requirements without developers, making it the most agile and borrower-friendly intake solution in 2026.

EasySend tends to deliver the highest value when:

- You already have a LOS (nCino, LendFoundry, Jack Henry, etc.) — and you don’t want to rip out or replace it.

- Your pain points are around borrower friction, document chaos (PDFs, emails), version control, slow condition-clearing, manual chasing.

- You need multi-party, conditional, loan-type-aware intake flows (e.g. commercial loans, guarantor agreements, co-borrowers, complex collateral docs).

- You want no-code/low-code flexibility so business teams can update document requirements, loan paths, and intake logic on the fly.

- You aim to deliver a modern, mobile-first, user-friendly borrower experience — reducing drop-offs and accelerating time-to-close.

nCino (Full loan origination system with built-In document manager)

nCino is an enterprise-grade LOS built on Salesforce, widely used by banks to unify commercial, small business, and retail lending in one cloud system. It centralizes underwriting, credit policies, risk assessment, and back-office workflows while offering a borrower portal for uploading and sharing documents.

The document manager allows institutions to configure checklists by product type and enforce compliance across loan files. Borrowers can upload documents, track status, and communicate through the portal, while staff manage files within a unified LOS environment.

However, because nCino’s borrower-facing experience is tied closely to LOS workflows and Salesforce objects, it offers limited flexibility compared to a dedicated front-end engine. Building highly customized, dynamic borrower journeys or complex multi-party workflows typically requires technical support or additional development. nCino works best as a strong core system—often complemented by EasySend for a modern, flexible intake layer.

Jack Henry (LoanVantage + Digital LOS Suite)

Jack Henry provides an integrated LOS that spans consumer, business, and commercial lending. The platform delivers standardized digital application flows and a document upload experience designed to replace paper-heavy processes inside community banks and credit unions.

Borrowers can apply online, upload supporting documents through secure channels, and track the progress of their application. For lenders seeking standardization across multiple loan types, Jack Henry provides a single system for processing, underwriting, and document management.

Where Jack Henry is strongest is centralizing loan lifecycle management—not offering highly customizable intake UX. Because customization typically requires vendor engagement, lenders with complex workflows or multi-party processes often augment Jack Henry with a flexible, no-code intake solution like EasySend to create dynamic borrower experiences without altering core infrastructure.

LendFoundry (Cloud-native LOS for digital lenders & Fintechs)

LendFoundry is a cloud-based LOS designed for modern fintech lenders seeking speed, automation, and modular digital origination. It includes a borrower portal, digital applications, automated document upload, and built-in eSignature—reducing reliance on manual intake channels.

Its strength lies in providing an end-to-end origination backbone with configurable loan products, underwriting automations, and borrower-facing portals. This makes it well suited for emerging lenders launching digital-first products.

However, customization of front-end UX and dynamic workflows is more limited compared to a dedicated intake engine. Lenders that want more advanced borrower journeys, conditional intake paths, or multi-party collaboration often layer EasySend on top of LendFoundry to deliver a superior, branded experience while keeping the LOS as the system of record.

Generic LOS with basic document portal (typical legacy or mid-market systems)

Many LOS platforms—especially legacy or mid-market solutions—include a basic document portal that allows borrowers to upload files, track tasks, and view status updates. These features usually meet minimum compliance requirements and provide a centralized repository for underwriting teams.

However, these portals are highly standardized and not designed for modern borrower expectations. They often lack:

- Dynamic, conditional flows

- Role-based experiences

- Multi-party support

- Real-time validation

- Modern mobile-first UX

- No-code customization

- AI-powered guidance

As a result, lenders rely on PDFs, email attachments, or manual workarounds that create friction for borrowers and slow down approvals. These LOS portals provide foundational functionality but rarely deliver the intuitive, fast, user-friendly experience that borrowers expect in 2026—especially for complex or commercial loans. EasySend is often added to modernize this intake layer without altering the LOS.

Custom or Legacy LOS + Manual Intake or Third-Party Upload Tools

Some lenders still operate on legacy LOS systems supplemented with a mix of tools—email, cloud storage, spreadsheets, or simple upload widgets. These fragmented workflows create confusion for borrowers and add significant manual workload for staff who must chase missing items, interpret documents, and enter data manually.

Custom-built intake tools or portal add-ons may provide incremental improvements, but they rarely support dynamic logic, multi-party journeys, eSignatures, or true no-code configurability. Maintaining these custom systems requires ongoing IT support and limits the lender’s ability to adapt quickly.

For organizations in this situation, EasySend provides a streamlined path to modernization: a ready-to-use, AI-powered intake layer that sits above legacy infrastructure, digitizes the entire borrower journey, and integrates cleanly into whatever LOS or CRM the lender already uses.

5. LOS vs. portal vs. interaction layer vs. AI: how they fit together

The Problem With Traditional LOS-Based Document Intake

Most lending organizations expect their Loan Origination System (LOS) to manage both underwriting and borrower-facing intake. But LOS platforms were never built to power modern digital customer experiences. Their portals are typically static, slow to update, and heavily dependent on PDFs—resulting in borrower frustration and operational inefficiency.

Common issues include:

- Rigid checklists that don’t adapt to borrower inputs

- Static, non-dynamic forms that overwhelm applicants with irrelevant questions

Limited multi-party logic, forcing borrowers, co-borrowers, and guarantors to email documents separately - Poor mobile experience, leading to drop-offs

- Heavy reliance on PDFs, which causes version issues and incomplete submissions

- Difficult or costly customization, requiring IT or vendor involvement

- Compliance risk when borrowers revert to email because portals are confusing

The result is predictable: slow cycle times, manual chasing, and an inconsistent borrower experience.

This is the gap EasySend fills—by becoming the digital interaction layer LOS platforms were never built to be.

Where EasySend Fits in the Modern Lending Technology Stack

EasySend doesn’t replace your LOS—it enhances it.

It sits at the front door of the lending process, orchestrating everything borrowers see while your LOS continues to manage underwriting, credit decisioning, and core workflows.

Here’s the modern architecture most lenders adopt:

Borrower → EasySend Digital Journey → LOS/CRM → Underwriting → Approval → Funding

This separation of responsibilities gives lenders speed, flexibility, and modernization—without replacing their core system.

Most LOS portals are built to manage compliance, not customer experience. EasySend delivers a dynamic, borrower-first intake layer.

This is why lenders with strong LOS systems still choose EasySend as the interaction and experience layer.

That is why most 2026 lending stacks that work really well follow a pattern like:

1. LOS – nCino, Jack Henry, MeridianLink, LendFoundry, etc.

2. Borrower / document portal – built-in (Blend, LendFoundry, Jack Henry) or add-on (FileInvite, SmartVault, Clustdoc).

3. Customer interaction & workflow engine – EasySend to orchestrate the borrower journey and multi-party workflows across channels and products.

4. AI document analysis – Ocrolus (and similar tools) to automate financial document review and condition clearing.

In that architecture, document intake becomes:

- Guided and dynamic (instead of static checklists)

- Multi-party and omnichannel

- AI-validated and decision-ready

- Tightly integrated with your LOS and CRM

6. How to choose the right platform mix

Here’s a simple decision cheat sheet:

Scenario A – You’re on an older LOS and still collecting docs via email

- Keep your LOS for now.

- Add a document portal specialist (FileInvite, SmartVault, Clustdoc) for secure uploads and basic automation.(fileinvite.com)

- Layer EasySend on top for dynamic, AI-powered borrower journeys and multi-party flows, and to integrate portal + LOS + CRM.(easysend.io)

- For higher volumes and complex files, add Ocrolus to automate document analysis.(Ocrolus)

Scenario B – You’re moving to a cloud LOS (nCino, LendFoundry, Jack Henry, MeridianLink)

- Use the native borrower portals and document-management modules from your LOS.(nCino)

- Layer EasySend as the customer interaction engine for complex mid-market and commercial flows, cross-sell journeys, and multi-brand experiences.(easysend.io)

Scenario C – You’re a digital lender/fintech building an end-to-end experience

- Start with a modern LOS (Blend + LOS partner, LendFoundry, similar cloud-native options).(Blend)

- Design the entire borrower and partner experience in EasySend to differentiate on UX, dynamic logic, and speed.(easysend.io)

- Use FileInvite or SmartVault only if you need standalone portals for specific use cases (e.g., existing business line with separate process).(Software Advice)

Conclusion: Document intake innovation will define lending leaders in 2026

Borrowers expect fast, intuitive digital experiences.

Underwriters need complete and clean data.

Compliance teams require auditability and control.

Banks need to move faster without ripping out core systems.

EasySend is the only platform that solves all of this at once—by becoming the dynamic, AI-powered customer interaction layer for loan origination.

It is not just another portal.

It is not just a form builder.

It is not an LOS replacement.

EasySend is the missing layer that unifies data intake, document collection, workflows, and digital experiences—end to end.

FAQ

Forget forms. Create digital customer journeys.