.avif)

Outlook

Recent trends in auto insurance suggest that one of the major areas ripe for disruption is auto insurance claims.

Manual claims processing is often seen as a necessary evil by both insurance carriers and policyholders alike. But what if there was a way to make claims processing easier, faster, and less error-prone?

This is where technology comes in. By harnessing the power of data and using it to streamline the claims process, auto insurance carriers can provide a much better experience for their customers while reducing costs.

What's In This Guide?

In this guide, we'll cover the following topics:

- The current state of auto insurance claims

- Recent trends in auto insurance claims

- How technology is changing the auto insurance claims landscape

- What carriers can do to improve their claims process

- The future of auto insurance claims processing

The current state of auto insurance claims

Auto insurance claims have been around for as long as there have been cars on the road, and while the claims process has gradually evolved over time, it has remained largely the same for many years.

Typically, when a policyholder files a claim, they must first submit a detailed report of the incident to their insurance carrier. The carrier then opens an investigation and may ask for additional information from the policyholder.

Once the carrier has all of the necessary information, they will determine whether or not the claim is valid and how much money should be paid out to the policyholder. If the policyholder is unhappy with the decision, they can file an appeal.

This process can take weeks or even months to complete, and is often seen as being slow, cumbersome, and opaque. As a result, policyholders frequently feel frustrated and dissatisfied with their experience.

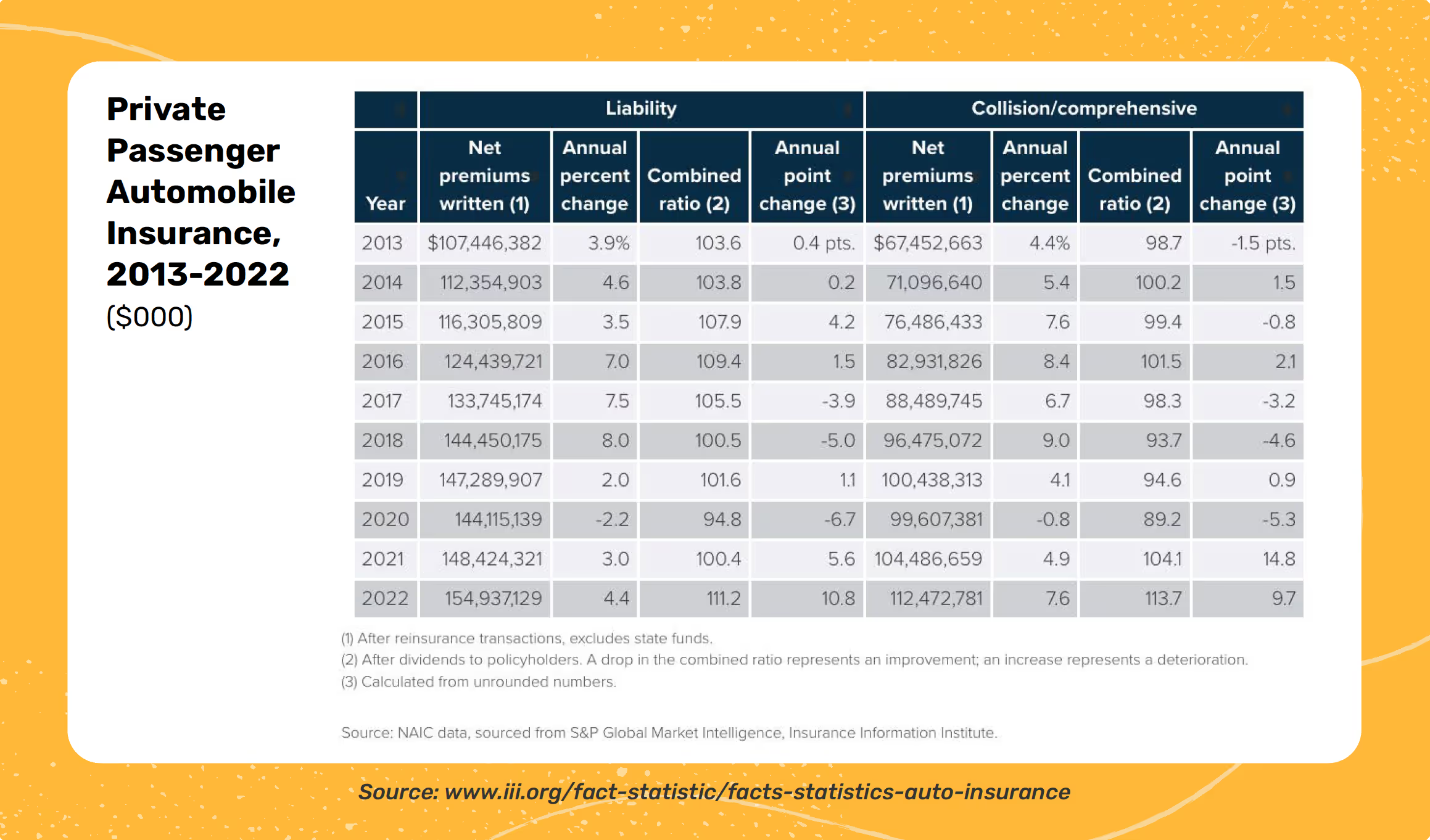

Key auto insurance statistics

- Nearly 270 million drivers carry car insurance in the U.S. (ValuePenguin)

- The market size, measured by revenue, of the Automobile Insurance industry was $348.9bn in 2022. (IBISWorld)

- The average cost of car insurance in the U.S. is expected to rise to nearly $1,900 by the end of 2023, representing a significant increase from previous years. This is a 16% increase compared to the beginning of the year (source: Autobody News).

- As of 2023, approximately 12.6% of all drivers in the U.S. are uninsured. This figure varies by state, with Mississippi having the highest percentage of uninsured drivers at 29.4%, and New Jersey the lowest at 3.1% (source: Policygenius).

- The national average cost of auto insurance is around $1,300 per year, varying based on several factors like location, age, gender, and driving history (Policygenius).

- The average person shops for car insurance every few years. Those who switch providers can save over $500 on average (Finder).

Recent Trends in Auto Insurance Claims

- Increase in Claims Frequency: There's been a steady rise in the number of claims filed since 2010 across various types of insurance claims (Insurance Information Institute (III)).

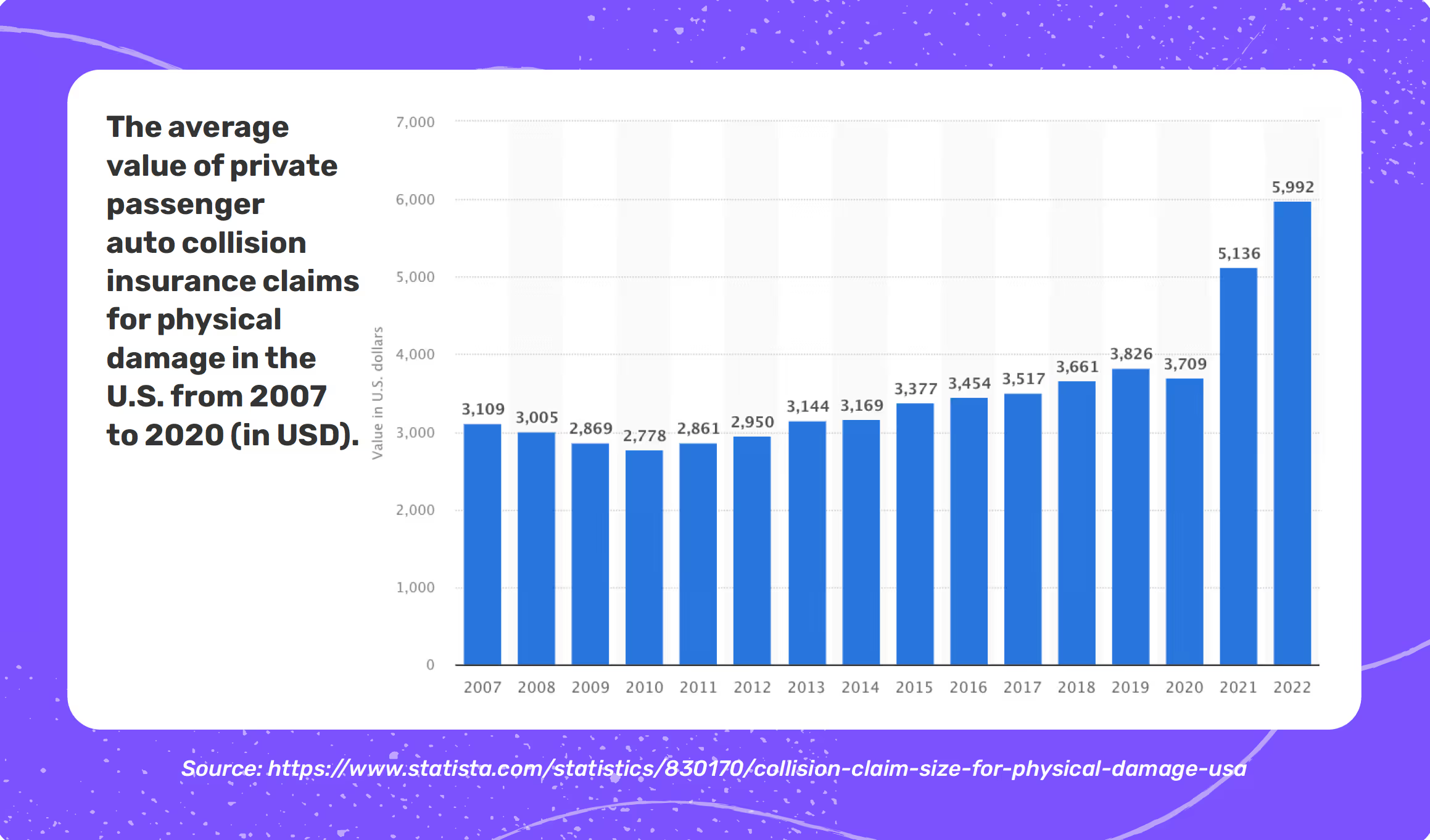

- Rising Insurance Payouts: The average cost of an auto insurance claim rose by 3.3% between 2018 and 2019, with the average private passenger auto collision claim for physical damage amounting to $5,992 in 2022 (Statista).

As of 2023, the landscape of auto insurance claims and costs in the U.S. has seen significant developments:

- Insurance costs vary significantly by state, with some states like Iowa and North Carolina being among the cheapest for full coverage, while states like Florida and Louisiana are among the most expensive. The cost of coverage also depends on several factors, including the level of coverage chosen by the policyholder.

- Despite car insurance being mandatory in most states, a notable percentage of drivers remain uninsured. For instance, Mississippi has the highest percentage of uninsured drivers at 29.4%, while New Jersey has the lowest at 3.1%.

- The cost of auto insurance premiums has increased over the years. According to the Consumer Price Index, the cost of car insurance has risen by an average of 3.9% per year since 2011. The most significant annual increase was observed in 2017, with a 7.7% rise.

- The affordability of auto insurance varies across states. States like Louisiana, Florida, and Michigan are less affordable, whereas Iowa is among the most affordable. This affordability is calculated based on the auto insurance expenditure share of income.

- There have been changes in claim frequency and severity for various types of insurance coverages, including liability, collision, and comprehensive insurance, over the years. For example, the claim frequency and severity for bodily injury and property damage under liability insurance, and physical damage under collision and comprehensive insurance, have seen fluctuations.

Recent trends in auto insurance claims

In recent years, various changes have taken place in the auto insurance claims landscape, driven by a number of factors including the rise of digital technologies, the effect of the global pandemic and supply chain shortages on driving patterns, and the growing number of car accidents.

The frequency of claims is on the rise

One of the most notable changes in auto insurance is the increase in the number of claims being filed which, according to data from the Insurance Information Institute (III), has risen steadily since 2010 across insurance claim types.

From a frequency standpoint, collision claims are most commonly filed at an average of 5.9 claims per 100 year of insured coverage on a vehicle. The second most frequent claims are property damage at 3.4, comprehensive at 2.8, and, least frequent, bodily injury at 1 claim per 100 car years.

The rise in insurance payouts

Insurance payouts are expected to increase due to the rising frequency and severity of claims. In a 2019 report, the III found that the average cost of an auto insurance claim rose by 3.3% between 2018 and 2019. While 2020 saw a slight drop, the pandemic-caused decrease in driving is not expected to have a significant effect on claims costs in the next years.

[.emph] 2021 saw sharp increase with claims surging to $5,136 per claim, a 32% increase [.emph]

This trend is likely to continue in the coming years as the frequency and severity of claims continue to rise.

In 2022, the average private passenger auto collision claim for physical damage amounted to $5,992 in the U.S. (Statista)

The average value of private passenger auto collision insurance claims for physical damage in the U.S. from 2007 to 2022 (in USD) source

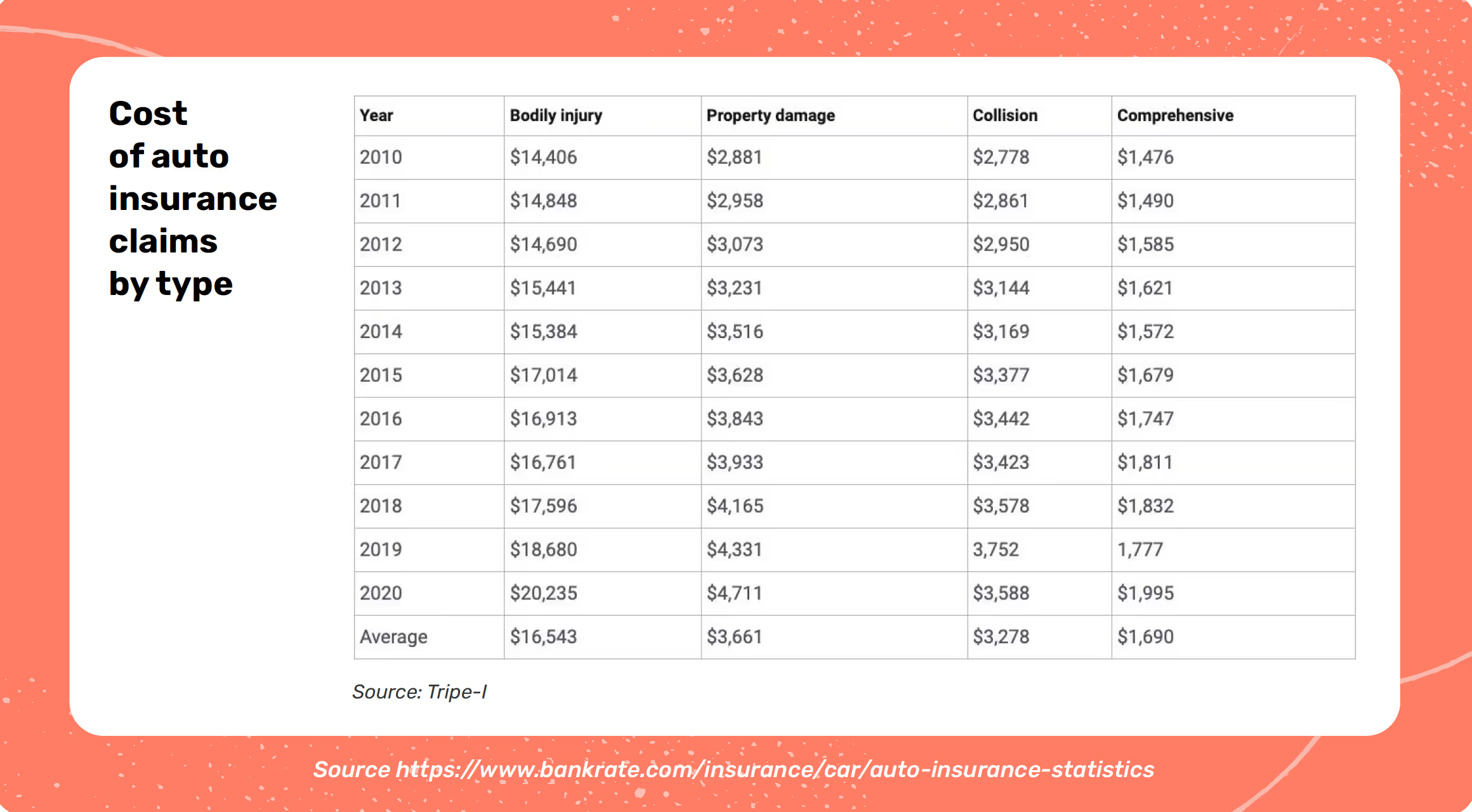

The four categories of auto insurance claims are bodily injury, property damage, collision, and comprehensive. Bodily injury and property damage claims are about liability or the policyholder’s responsibility to others for property damage or bodily injury. Collision and comprehensive claims cover damage and theft to the policyholder’s car.

Unsurprisingly, bodily injury claims are the most expensive, at an average of $20,235 per loss, followed by property damage at $4,711, collision at $3,588, and comprehensive are the least expensive at $1995.

Rising cost or repairs

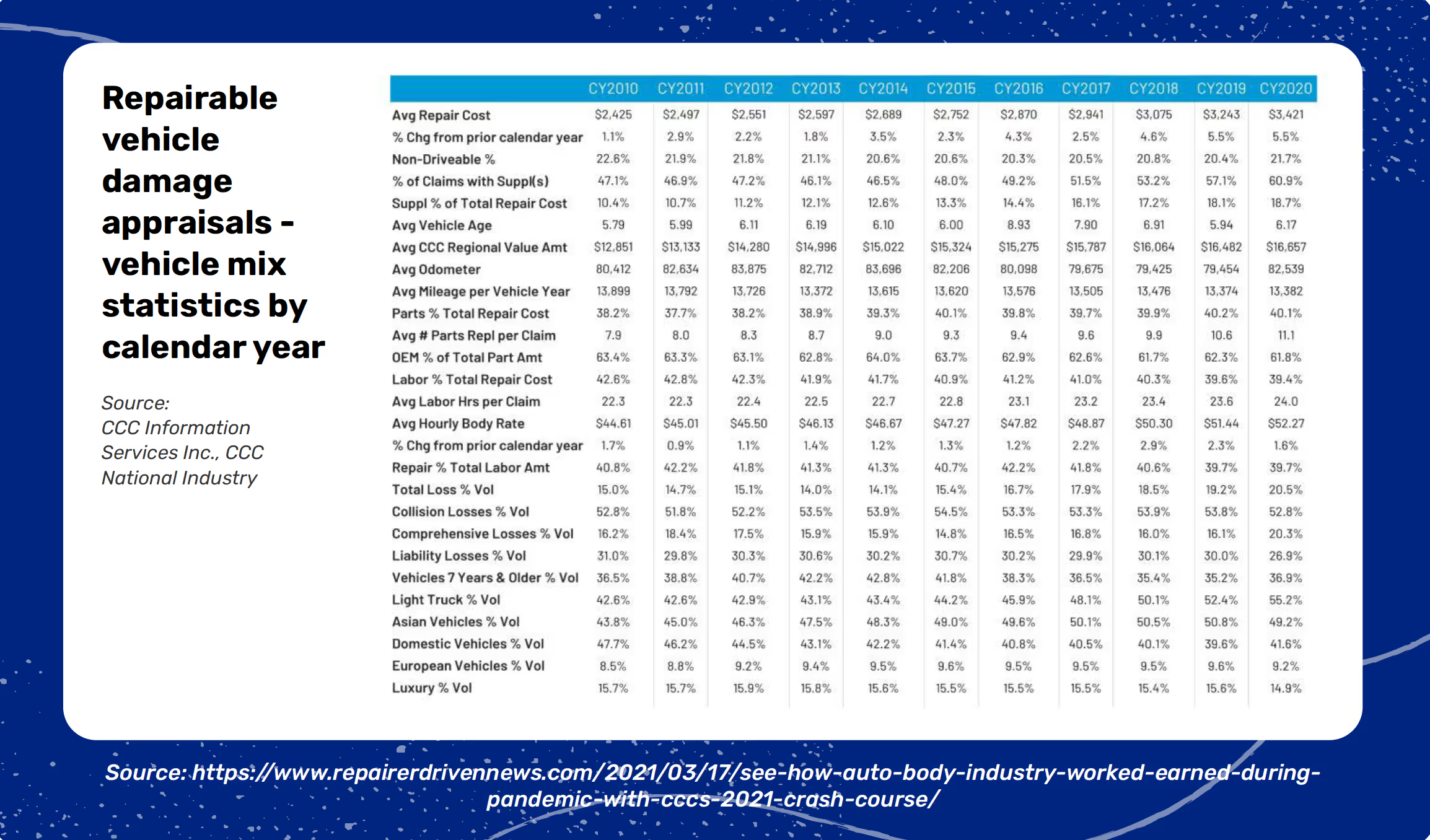

One of the biggest drivers of increased payouts is the cost of repairs, which has been rising steadily for many years. According to the National Insurance Crime Bureau, the average cost of auto body repairs rose by 4.1% from 2018 to 2019.

This trend is likely to continue in the future as the cost of labor and parts continue to increase.

The average cost of auto body repairs in the U.S. rose from $2,425 in 2010 to $3,421 in 2020 (in USD).

The threat of new entrants

Another factor that is affecting the industry is the threat of new entrants into the market. In recent years, a number of new players have entered the auto insurance claims space, offering policyholders a more streamlined and efficient claims process.

The impact of technology on user expectations

Technology is also having a major impact on the auto insurance claims landscape. Today's policyholders are more tech-savvy and expect a more streamlined and efficient claims experience. As a result, insurance carriers are turning to technology to improve the claims process.

Research shows that 40% of drivers who submit a claim are likely to switch insurers within the year (ims).

According to recent study, insurance customers ranked the following as the top three areas where they would like to see improvements in the claims process:

- Seamless customer experience

- Reducing the amount of time it takes to resolve a claim

- Improving communication throughout the claims process

How technology is changing the auto insurance claims landscape

Auto insurance has undergone tremendous changes due to technological advancements and changing customer needs. As we move into 2023, the auto insurance industry will continue to be shaped by these factors.

Here are some of the key trends that we expect to see in the coming years in auto claims. The areas we expect to be transformed by technology are:

- First notice of loss (FNOL): Claimants will increasingly use digital channels such as chatbots and virtual assistants to report their claims. This will allow insurers to gather information more quickly and efficiently and could help to reduce fraud.

- Claims adjusting: The use of artificial intelligence (AI) will continue to grow in importance in claims adjusting. AI-powered chatbots and virtual assistants can help to speed up the claims process by automating routine tasks such as data gathering and customer communication.

- Fraud detection: Machine learning will be used increasingly to detect and prevent fraud. By analyzing large data sets, insurers can identify patterns of fraud and take steps to stop it before it happens.

- Customer experience: Policyholders are increasingly demanding a more seamless and efficient experience. In response, insurers are turning to technology to automate and improve claims handling.

In order to stay ahead of the curve, streamline the process and make it more efficient, insurers need to embrace these changes and adopt new technologies. Those who don’t will risk being left behind.

Steps in auto claims workflow

Insurers typically have a goal of settling and paying your claim within 30 days, following the Standards for Prompt, Fair and Equitable Settlements.

There are a few key steps in the auto insurance claims workflow:

- First notice of loss: The policyholder notifies the insurer of the incident, typically via phone or online.

- Data gathering: At this stage, the insurer will collect information about the incident, including photos, police reports, and witness statements.

- Investigation and assessment: The adjuster will investigate the claim and assess the damages.

- Estimate: The insurer will generate an estimate.

- Settlement: Once the damages have been assessed, the insurer will make a settlement offer to the policyholder.

- Payment: Once the repairs have been completed, the policyholder will be reimbursed by the insurer.

- Appeals: If the policyholder is not satisfied with the settlement offer, they can file an appeal.

- Repair: If the policyholder decides to repair their vehicle, the insurer will reimburse them for damages up to the agreed-upon amount.

- Post-settlement follow-up: 40% of insured car owners switch insurers after filing a claim. It is imperative to maintain regular communication with the customer

Why does it take so long to process a claim?

Customers want their claims handled promptly and efficiently, with as little hassle as possible. Yet, claims remain to be one of the most complex and time-consuming tasks for insurers. Common issues that cause delays include:

Incomplete or inaccurate data

One of the biggest challenges in claims processing is incomplete or inaccurate data. This can be caused by human error, such as incorrect information being entered into the system, or by a lack of data integration between different systems.

One of the most common delays is when the customer doesn't provide all of the required information, delaying the entire process.

Lack of communication

Another common issue is a lack of communication between different departments within the insurer, or between the insurer and the policyholder.

Insurance claims aren't dependent on just one person. The process involves multiple parties who must provide the required information. This can lead to delays in the claims process as information is passed back and forth.

For example, to process the claim, the insurer needs to get data and documents from multiple parties, including:

- The policyholder

- The customer support agents who receive FNOL from policyholders must be available to assist and answer questions

- The claims adjusters

- The body shop needs to be available to work with both the insured and the claims adjuster

- The hospital and doctor's office should coordinate directly with the car insurance personal injury claims adjuster

- Health insurers typically file their own claim with the car insurance company of the at-fault driver to seek reimbursement

If one of the players isn't cooperating, the entire process can get delayed. Without proper collaboration, a claim can get dragged out.

Lack of resources

Adjusters are often overloaded with work, which can lead to delays in processing claims. Oftentimes, insurers are simply understaffed and lack the resources to keep up with the demand.

Complex processes

The insurance claims process is notoriously complex, with many different steps that must be completed in a specific order. This can make it difficult to keep track of where the claim is.

There are different types of coverage that can complicate the claims process. For example, if you have both collision and comprehensive coverage, the insurer will first determine which type of coverage is applicable to the claim.

If you have multiple vehicles on your policy, the insurer will also have to determine which vehicle was involved in the accident.

Different claims require different workflows

There is a wide variety of workflows between different types of claims, for example, damage claims have a very different workflow than medical claims, andbodily injury liability claims have a different workflow than uninsured motorist bodily injury claims. This can lead to confusion and delays.

Common types of claims:

- Roadside Assistance Claim

- Glass Claim

- Physical Damage

- Total-Loss Claim

- Medical Claim

Fraud prevention

Another reason why claims can take a long time to process is that the insurer wants to be thorough and to make sure that the claim is legitimate with no fraud involved. This adds extra steps and therefore delays claims workflows.

What can be done to speed up the claims process in auto insurance?

As customers become more demanding, insurers need to find ways to improve the claims process.

Top technologies transforming auto claims in 2023:

- Artificial intelligence (AI)

- Chatbots

- Robotic process automation (RPA)

Each of these technologies can help improve the claims process in different ways.

- Artificial intelligence (AI) can be used to help sort and categorize claims, identify fraud, automate the claims process, and speed up decision-making.

- Chatbots can be used to communicate with customers and gather information about their claims.

- RPA can be used to automate repetitive tasks associated with the claims workflow.

Yet, to fully take advantage of these technologies, insurers must first transform the way they collect data.

The problem: manual data collection methods

One of the main reasons for missing data and delays is that insurers typically rely on manual data collection methods, such as phone calls, paper forms, and in-person meetings.

The way data is collected for auto insurance claims is often manual and paper-based. This means that a lot of data needs to be entered into the system manually. This can be time-consuming and often leads to errors.

It also takes a lot of time to collect all the required information from different parties. This can delay the claims process significantly, creating a huge challenge for insurance companies.

Digital data collection is a must for digital transformation

Digital data collection is essential for insurers who want to improve the claims process. By gathering data digitally from the get-go, insurers can take advantage of technology to automate routine tasks and utilize data analytics, making the process more efficient and improving the customer experience.

There are multiple advantages to digital data collection:

- Prevent errors: When information is entered manually, there is a greater chance for mistakes. This can cause delays as the claims adjuster will have to track down the correct information.

- Ensure that data is complete: Ensure that all required data and documents are presented at the point of entry to avoid having to go back to the customer to gather missing data.

- Make it easy to share information between parties: When information is digital, it can be easily shared with all the parties involved in the claims process.

- Automate workflows: Digitally collected data can be automatically routed to the appropriate adjuster or vendor, speeding up the claims process. Automating workflows makes it easier for adjusters to assess damages and generate estimates.

- Reduce fraud: Digital data collection empowers insurers to reduce fraudulent claims by allowing insurers to verify data in real-time and compare it against historical data.

- Integrate with internal systems: When data is digital, it can be easily integrated with internal systems such as policy administration, claims, and billing. This allows for a seamless customer experience.

Transforming data collection leads to efficiency gains downstream in the claims process, transforming the entire workflow and enabling automation and efficiency gains.

Digital transformation requires digital data

The bottom line is that insurers need to embrace digital data collection if they want to improve the auto insurance claims process. Digital data collection enables automation, which leads to efficiency gains throughout the entire process.

The customer's journey begins long before they ever have to make a claim. In order to provide the best possible experience, insurers need to focus on the entire customer lifecycle, from quote to claim. By understanding the customers’ needs at each stage of their journey, insurers can proactively address any pain points and prevent them from becoming dissatisfied.

What's next for auto insurance claims?

The auto insurance industry is under pressure to improve the claims process. In the coming years, we expect to see more insurers adopt new technologies to speed up the process and improve customer satisfaction.

Digital data collection is essential for insurers who want to improve the end-to-end customer journey. By gathering data digitally from the get-go, insurers can take advantage of technology to automate routine tasks and utilize data analytics, making the process more efficient and improving the customer experience.

.avif)

.avif)

.avif)