TL;DR

A digital loan document intake workflow is a guided, end-to-end journey—not a static form or upload portal. It adapts in real time to borrower input, requests documents contextually, validates data as it’s entered, coordinates multiple participants automatically, and syncs everything directly into systems like Salesforce and the LOS. The result is faster completion, cleaner data, and significantly lower operational overhead.

Most lenders agree on the goal: faster applications, cleaner data, fewer follow-ups.

Where many still struggle is execution—specifically, how loan documents are actually collected, validated, coordinated, and delivered into core systems.

A truly digital loan document intake workflow is not a portal with upload buttons. It is not a static checklist. And it is not a form with a submit button at the end.

A modern workflow is a guided, end-to-end journey that adapts in real time, connects directly to systems like Salesforce and the LOS, and ensures every piece of data ends up exactly where it belongs.

This is what that workflow looks like in practice.

Step 1: Intake starts with a journey, not a form

In a modern setup, document intake does not begin with a blank application form. It begins with a contextual, personalized journey.

Borrowers are invited into a guided experience that already “knows” who they are and why they are there—whether they are applying for a loan, renewing a lease, submitting a claim, or completing onboarding. The experience adapts immediately based on known data from Salesforce or another system of record.

Instead of asking for everything upfront, the journey reveals steps progressively. Questions, document requests, and signatures appear only when relevant. This reduces friction for borrowers and prevents unnecessary data collection that leads to confusion or abandonment.

This is the foundational shift: from field capture to guided completion.

Step 2: Documents are requested contextually and validated in real time

In traditional workflows, documents are treated as attachments. Borrowers upload files, operations teams review them later, and the inevitable back-and-forth begins.

In a digital intake workflow, documents are treated as structured inputs tied to logic.

As the borrower moves through the journey, document requests are triggered dynamically based on their answers. A self-employed applicant is guided down a different path than a salaried one. A co-borrower is introduced only when required. Supporting documents are requested at the moment they make sense—not all at once.

Crucially, validation happens immediately. Missing pages, incorrect formats, incomplete signatures, or inconsistent information are flagged before the borrower can proceed. This dramatically reduces rework and ensures that what reaches underwriting or operations is already decision-ready.

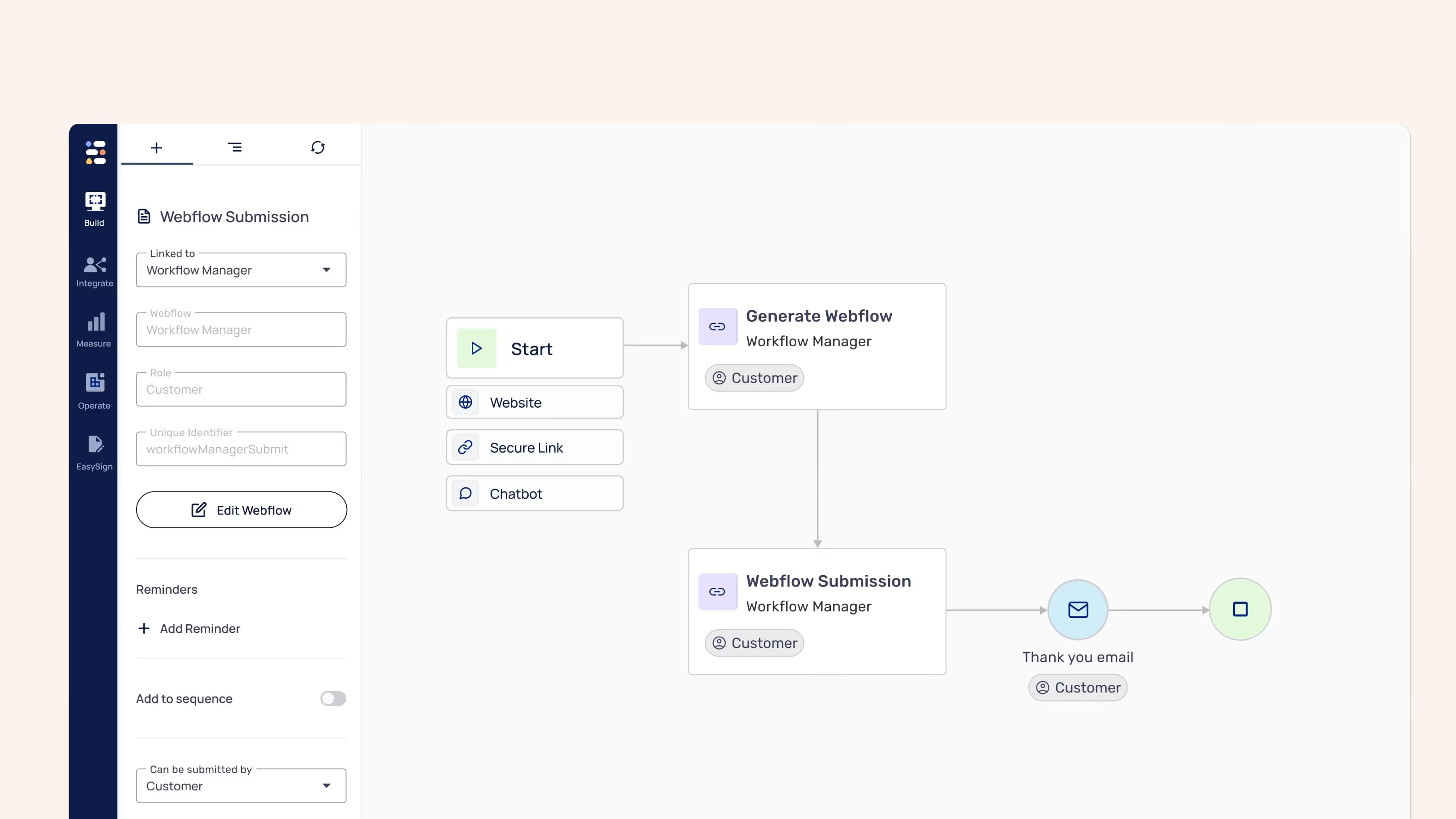

Step 3: Multi-party coordination happens automatically

Loan applications rarely involve a single participant. Co-borrowers, guarantors, internal approvers, and reviewers are often part of the process.

In legacy setups, this coordination is manual. Emails are sent. Status is tracked in spreadsheets. Teams chase signatures and uploads across systems.

A modern digital workflow orchestrates this automatically.

Each participant is invited at the right time, sees only what is relevant to them, and completes their part without confusion. Dependencies are enforced by the workflow itself, not by human follow-up. Progress is visible in real time, both to the borrower and to internal teams.

The result is a process that moves forward predictably instead of stalling at handoffs.

Step 4: eSignatures are embedded, not bolted on

In many loan processes, eSignatures are treated as a final, disconnected step. Documents are generated, emailed, signed, and then manually reconciled back into the system.

In a modern intake workflow, signatures are part of the journey.

They appear in context, after all required data and documents are complete. Signatures can involve multiple parties, sequentially or in parallel, without breaking the flow. The signed output is automatically linked to the correct record and routed to the right system.

This eliminates one of the most common sources of delay at the end of loan applications.

Step 5: Data flows directly into Salesforce and core systems

A digital document intake workflow only delivers value if data lands where teams actually work.

In a modern setup, journeys are connected directly to Salesforce and downstream systems. As borrowers complete steps, data is synced in real time to the appropriate objects—leads, accounts, opportunities, cases, or custom records. Documents and signatures are attached correctly. Status updates are visible instantly.

This allows teams to launch, manage, and monitor loan intake entirely inside Salesforce, without switching tools or reconciling data manually.

The workflow becomes part of daily operations, not a parallel process.

Step 6: AI accelerates creation and iteration

One of the biggest bottlenecks in modernizing intake workflows has historically been setup time. Designing logic, building flows, and maintaining variations often required technical resources.

AI changes this dynamic.

With EasySend AI, teams can create complete digital journeys in seconds—either by describing the process in natural language or by converting an existing PDF into a live, guided journey. What once took weeks can now be done in minutes, without sacrificing control or compliance.

This makes it realistic to evolve workflows continuously as products, regulations, or customer expectations change.

What changes for the business

When document intake becomes a guided, system-connected workflow, the impact is measurable.

Organizations using EasySend report significant improvements across adoption, speed, and cost. Customer adoption increases because journeys are easier to complete. Sales and approval cycles shorten because data arrives complete and validated. Operational costs drop as manual follow-ups and corrections are eliminated.

In some cases, the savings are substantial—hundreds of thousands of dollars annually—simply by removing inefficiencies from intake.

Just as importantly, teams regain control over their processes. Business users can iterate without waiting on development cycles, while IT maintains governance and integration integrity.

Security and compliance are built in, not added later

Loan document intake involves sensitive personal and financial data. Any digital workflow must meet strict security and compliance requirements from day one.

Modern intake platforms are designed with enterprise-grade standards at their core, supporting regulations and frameworks such as GDPR, SOC 2, ISO 27001, PCI DSS, SSO, OTP, and HIPAA where applicable.

This ensures that innovation at the front door does not introduce risk downstream.

The future of loan document intake

The future of loan origination is not defined by better forms or prettier portals. It is defined by intelligent, connected workflows that guide borrowers, validate data in real time, coordinate participants automatically, and integrate seamlessly with core systems.

A digital loan document intake workflow is no longer a nice-to-have. It is the foundation for faster decisions, lower costs, and better customer experiences.

The lenders who move from forms to journeys will not just digitize existing processes—they will fundamentally outperform those who do not.

FAQ

Forget forms. Create digital customer journeys.