Credit unions have been a reliable and trusted source of financial services for decades. However, as technology advances and the banking landscape evolves, credit unions must stay ahead of the curve and create innovative ways to serve their members.

Competitive pressures and challenging landscape

Credit unions are facing increased competition from other financial institutions, including large banks, fintech startups, and online lenders. These competitors are gaining market share by offering more attractive rates, fees, and digital services, which could make it harder for credit unions to retain their members.

At the same time, credit unions face a complex regulatory environment that could lead to compliance costs and operational burdens. New regulations, such as the NCUA’s new risk-based capital rule and the CFPB’s proposed changes to the Qualified Mortgage (QM) Rule, could also impact credit unions’ ability to serve their members.

Another challenge is the changing member demographics, including the preferences and expectations of younger generations, such as Millennials and Gen Z. These groups demand more personalized digital experiences, mobile banking options, and socially responsible investments.

The macroeconomic environment can impact credit unions in various ways, including loan demand, delinquency rates, and interest rates. Fluctuations in the economy could also impact credit union investment portfolios and liquidity positions.

To be successful in light of all these challenges, credit unions need to go beyond just offering competitive rates and a robust product portfolio. They must provide an outstanding experience that meets the needs of their members and exceeds their expectations.

To achieve their goals, credit unions must continue to invest in new technology to remain competitive and to meet member expectations for digital services. This could involve updating legacy systems, implementing new mobile banking apps, and improving data analytics capabilities.

Digital data intake for better member experience

One powerful way credit unions can improve member experience and drive growth is by leveraging digital data collection.

Digital customer data intake is acquiring digital data from customers through digital channels such as websites, mobile apps, and social media. This data can be used to improve customer experience, personalize marketing messages, and understand customer behavior.

Manual data intake is a slow and labor-intensive process that hinders credit union competitiveness. Manual data entry causes delays and inefficiencies, resulting in higher costs and longer processing times. As the banking landscape becomes increasingly competitive, credit unions must be able to quickly acquire and utilize customer data.

The processes in credit unions that can benefit from transforming from manual to digital data intake include:

- Member onboarding

- Account maintenance

- Account opening

- Loan application processing

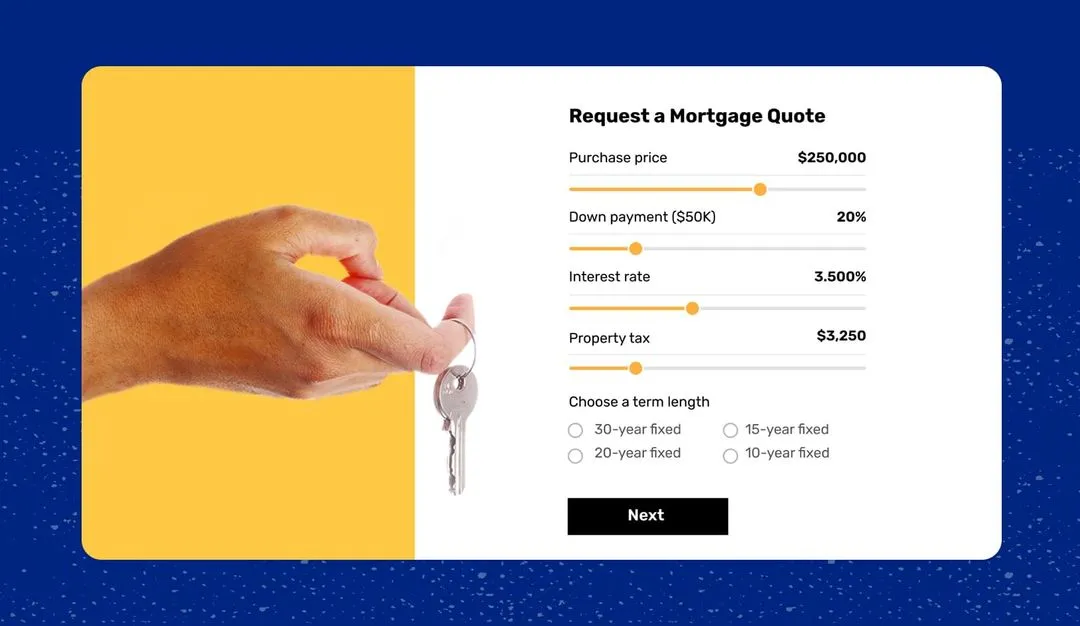

- Mortgage application processing

- Credit card applications

- Insurance products sales

- Financial transaction tracking

- Fraud detection and prevention

Digital data intake can make the customer onboarding process faster and more streamlined.

Advantages of digital data intake for credit unions

- Improved customer experience: Digital data collection can help credit unions understand their members’ needs and preferences and use this information to provide more personalized services and products.

- Increased efficiency: Digitally collecting customer data eliminates manual entry errors, which leads to faster decision-making processes and improved operational efficiencies.

- Better analytics: Credit unions can use the data they collect to gain insights into customer behavior, preferences and needs. This can help them make more informed decisions about product development, marketing strategies, and risk management.

- Competitiveness: Leveraging digital data collection can help credit unions stay competitive in the banking landscape by offering better services to their members.

- Real-time sync: Digital data collection allows credit unions to synchronize customer information in real-time, ensuring accurate and up-to-date data is always available and is not locked in siloed and isolated systems.

The bottom line: digital is the future

Manual and paper-based processes will no longer cut it in the digital age. Credit unions should embrace digital data collection and transform manual input to streamline member onboarding, loan applications, and other processes that require data entry. This will reduce costs and enhance convenience for members by eliminating manual steps in their journey with the credit union.

Data can also be used to provide more personalized experiences and offerings tailored to each member’s preferences. This allows credit unions to offer products and services that are more likely to be accepted by members and can reduce the cost of acquisition for new customers.

With digital data collection, credit unions can improve the member experience while also driving growth and staying competitive in this ever-changing landscape.

FAQ

Forget forms. Create digital customer journeys.